Estimating an RBC Model with a Stochastic Trend#

Real macro time series have trends. US per-capita real GDP, consumption, investment, and the capital stock have all grown at roughly 2% per year for over a century, so the raw data does not fluctuate around a constant mean. The plain RBC model from the previous notebook (Fitting an RBC to US Data) has no growth at all — its steady state is a single point, and every endogenous variable is stationary around it. To use that model with real data we had to remove the trend ourselves: log everything, fit a quadratic trend by OLS, and feed the residuals into the Kalman filter. That works, but it has two unattractive features:

It separates trend and cycle by hand. Any signal the trend regression absorbs is lost to the structural model — the DSGE never sees it, so it can’t tell us anything about it.

It commits us to a trend specification that has nothing to do with economics. A quadratic-in-time trend is convenient but arbitrary; the data did not generate themselves that way.

The cleaner alternative is to let the model itself produce the trend. We add a stochastic trend to productivity: a permanent random-walk-with-drift component on top of the usual stationary AR(1) shock. The deterministic drift \(g_z\) becomes an estimable parameter — interpretable as “the gross trend growth rate of this economy” — and trend innovations are real, permanent shocks that show up in the impulse response just like any other shock. After a change-of-variables that divides every trending quantity by the permanent productivity level, the model becomes stationary again and we can solve and estimate it with the same Kalman-filter / log-linearization machinery as the textbook RBC. The estimation is now joint: trend growth and business-cycle parameters are recovered together from the raw (logged) data.

A trend alone is not enough, though. A bare RBC with a single TFP shock cannot reproduce the joint dynamics of six macro series at once — there is one source of stochastic variation and six things to explain, so the Kalman filter will inevitably hand most of the action to measurement error. To give the model a fighting chance we add three standard real frictions (consumption habit, quadratic investment adjustment cost, variable capital utilisation) and four more structural shocks (preference, labour-disutility, investment, and utilisation-cost shocks). The result is a six-shock, six-observable model: exactly identified before measurement error, with enough flexibility to capture both the trend and the cycle in the French national-accounts data we’ll fit it to.

This notebook walks through the model end-to-end: the equations, the change-of-variables, parser and steady-state checks, then estimation with PyMC.

This notebook uses one package that is not a declared dependency of gEconpy. Install it into the same environment before running the cells below:

pip install eurostat

eurostat pulls quarterly French national-accounts and labour-force series directly from Eurostat’s SDMX API.

Model Equations#

Agents and primitives#

A representative household maximises expected discounted log utility over consumption and labour. Consumption enters with external habit (\(\phi_H\)), and the labour-disutility weight \(\Theta_t\) and the discount factor \(\beta_t\) are themselves AR(1) shock processes:

The flow budget constraint and the capital law of motion both pick up new pieces. The household pays a utilisation cost \(\Psi(z_t)\) for running its capital harder than steady state, and physical capital is delivered with a quadratic investment adjustment cost governed by \(\gamma_I\) and the investment-specific shock \(\xi^I_t\):

The utilisation-cost function is convex with its own AR(1) shifter \(\xi^\psi_t\), and its linear coefficient \(\psi_{z,1}\) is pinned to \(r^{ss}\) so the steady-state utilisation rate is exactly one:

A representative competitive firm produces output with Cobb–Douglas technology, labour-augmenting productivity, and capital services \(K^d_t = z_t K_{t-1}\) that respond to the household’s utilisation choice:

Productivity has two components, one stationary and one non-stationary:

\(A_t\) is a standard AR(1) wedge that reverts to one. \(Z_t\) is a random walk with drift \(\log g_z\), so it has a unit root and any innovation \(\varepsilon_{z,t}\) permanently shifts the productivity level. The deterministic drift \(g_z\) is the gross trend growth rate of the economy.

The full set of structural shocks#

There are six exogenous AR(1) wedges:

Shock |

State |

Reverts to |

Acts on |

|---|---|---|---|

\(\varepsilon_{A,t}\) |

\(A_t\) |

\(1\) |

Stationary TFP wedge in production |

\(\varepsilon_{z,t}\) |

\(G_t\) |

\(g_z\) |

Trend growth rate of productivity |

\(\varepsilon_{\beta,t}\) |

\(\beta_t\) |

\(\beta\) |

Discount factor / inter-temporal preference |

\(\varepsilon_{\Theta,t}\) |

\(\Theta_t\) |

\(\Theta\) |

Weight on labour disutility |

\(\varepsilon_{I,t}\) |

\(\xi^I_t\) |

\(1\) |

Investment adjustment cost |

\(\varepsilon_{\psi,t}\) |

\(\xi^\psi_t\) |

\(1\) |

Capital utilisation cost |

With six observables (\(Y\), \(C\), \(I\), \(L\), \(w\), \(r\)) and six shocks the state space is exactly identified — measurement error is now a modelling choice, not a structural requirement.

Why we cannot solve this directly#

Because \(Z_t\) has a unit root, every level variable that uses it as an input — \(Y_t\), \(C_t\), \(I_t\), \(K_t\), \(W_t\) — is non-stationary. The model has no point steady state in levels: it has a balanced growth path (BGP) on which all of these variables grow at rate \(g_z\). The linear perturbation tools gEconpy uses (and the Kalman filter, for that matter) require a stationary system. We therefore rewrite the model in deviations from the BGP by performing a change-of-variables.

Change-of-variables#

Define growth-adjusted (stationary) versions of each trending quantity by dividing through by \(Z_t\):

\(L_t\), \(r_t\), \(A_t\), \(z_t\), and all of the shock states are already stationary. The only piece of the trend that survives the transformation is the gross growth rate

so \(Z_t\) itself never appears in the stationary model — only \(G_t\) does. Applying the transformation to each equation gives the form actually written in the GCN file:

Production.

The factor \(1/G_t\) appears because predetermined capital was scaled by yesterday’s \(Z\), but today’s production uses today’s \(Z\).

Capital LOM with adjustment cost.

Subtracting \(g_z\) inside the quadratic centres the friction on the BGP investment growth rate, so the cost is exactly zero in steady state.

Budget constraint with utilisation cost.

Stochastic Euler equation (this is what the parser will derive from the household’s Bellman, with habit and the time-varying \(\beta_t\) folded in):

where \(\lambda_t\) is the budget-constraint multiplier and \(q_t\) the Tobin’s-\(q\) multiplier on the capital LOM. Habit makes \(\lambda_t\) depend on both current and lagged consumption.

Why log utility?#

With separable additive CRRA preferences

the change-of-variables introduces a \(Z_t^{1-\sigma_C}\) factor inside the discounted sum that does not drop out of the FOCs unless \(\sigma_C = 1\). King, Plosser, and Rebelo (1988) showed that BGP-compatible preferences either take the log form used here or a non-separable “KPR” form. Log utility is the simplest choice, and the only thing that changes when we layer habit and time-varying \(\beta_t / \Theta_t\) on top is that the FOCs pick up extra terms — the BGP-compatibility argument is unaffected.

Steady state#

At the BGP we set \(A = 1\), \(G = g_z\), \(z = 1\), all shock states equal to one, and constant lowercase variables. The frictions all vanish (zero adjustment-cost residual, zero utilisation cost), and the Euler equation collapses to

unchanged from the frictionless growth model. The capital law of motion gives

i.e., on the BGP, investment must cover both depreciation and the “dilution” of \(k = K/Z\) caused by growth in the denominator. The marginal utility of consumption now reflects habit:

The remaining ratios \(k/L\), \(y/L\), \(c/L\), \(w\), and the implied \(L^{ss}\) follow from the firm’s first-order conditions, the resource constraint, and the labour-supply FOC with the habit-adjusted \(\lambda^{ss}\). Closed forms for all sixteen steady-state quantities are given in the STEADY_STATE block of the GCN file.

import arviz as az

import arviz_plots as azp

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import preliz as pz

import pymc as pm

import gEconpy as ge

import gEconpy.plotting as gp

gp.set_matplotlib_style()

Loading the Model#

The growth-adjusted equations above are encoded in RBC_with_growth.gcn. gEconpy parses the file, derives the household and firm first-order conditions symbolically, and exposes a Model (for solving / simulating / IRFs) or a PyMCStateSpace (for Kalman-filter estimation in PyMC). Let’s first print the file so the model is in plain sight as we work through it.

gcn_path = "../GCN Files/RBC_with_growth.gcn"

ge.print_gcn_file(gcn_path)

Block: HOUSEHOLD

Definitions

\[u_{t} = - \frac{L_{t}^{\sigma_{L} + 1} \Theta_{t}}{\sigma_{L} + 1} + \log{\left(- \frac{\phi_{H} C_{t-1}}{G_{t}} + C_{t} \right)}\]

\[\Psi_{z t} = shock_{\psi t} \left(\frac{\psi_{z} \left(z_{t} - 1\right)^{2}}{2} + \psi_{z 1} \left(z_{t} - 1\right)\right)\]

\[adj_{cost t} = - \frac{\gamma_{I} \left(g_{z} - \frac{G_{t} I_{t} shock_{I t}}{I_{t-1}}\right)^{2}}{2} + 1\]

Controls

\[\operatorname{Set}\left(\left[ C_{t}, \ L_{t}, \ I_{t}, \ K_{t}, \ z_{t}\right]\right)\]

Objective

\[U_{t} = U_{t+1} \beta_{t} + u_{t}\]

Constraints

\[C_{t} + I_{t} + \frac{K_{t-1} \Psi_{z t}}{G_{t}} = L_{t} W_{t} + \frac{K_{t-1} r_{t} z_{t}}{G_{t}}\]

\[K_{t} = I_{t} adj_{cost t} - \frac{K_{t-1} \left(\delta - 1\right)}{G_{t}}\]

Identities

\[\log{\left(\beta_{t} \right)} = \rho_{\beta} \log{\left(\beta_{t-1} \right)} + \epsilon_{\beta t} - \left(\rho_{\beta} - 1\right) \log{\left(\beta \right)}\]

\[\log{\left(\Theta_{t} \right)} = \rho_{\Theta} \log{\left(\Theta_{t-1} \right)} + \epsilon_{\Theta t} - \left(\rho_{\Theta} - 1\right) \log{\left(\Theta \right)}\]

\[\log{\left(shock_{I t} \right)} = \rho_{I} \log{\left(shock_{I t-1} \right)} + \epsilon_{I t}\]

\[\log{\left(shock_{\psi t} \right)} = \rho_{\psi} \log{\left(shock_{\psi t-1} \right)} + \epsilon_{\psi t}\]

\[R_{f t} + 1 = \frac{G_{t+1} \lambda_{t}}{\beta_{t} \lambda_{t+1}}\]

Shocks

\[\operatorname{Set}\left(\left[ \epsilon_{\beta t}, \ \epsilon_{\Theta t}, \ \epsilon_{I t}, \ \epsilon_{\psi t}\right]\right)\]

Calibration

\[\beta = 0.99\]

\[\delta = 0.025\]

\[\sigma_{L} = 2.0\]

\[\phi_{H} = 0.6\]

\[\gamma_{I} = 6.0\]

\[\psi_{z} = 0.2\]

\[\psi_{z 1} = \delta - 1 + \frac{g_{z}}{\beta}\]

\[\Theta = 1\]

\[\rho_{\beta} = 0.9\]

\[\rho_{\Theta} = 0.9\]

\[\rho_{I} = 0.9\]

\[\rho_{\psi} = 0.9\]

Block: FIRM

Controls

\[\operatorname{Set}\left(\left[ K_{d t}, \ L_{t}\right]\right)\]

Objective

\[TC_{t} = - K_{d t} r_{t} - L_{t} W_{t}\]

Constraints

\[Y_{t} = A_{t} K_{d t}^{\alpha} L_{t}^{1 - \alpha}\]

Identities

\[mc_{t} = 1\]

\[K_{d t} = \frac{K_{t-1} z_{t}}{G_{t}}\]

Calibration

\[\alpha = 0.3\]

Block: EXOGENOUS

Identities

\[\log{\left(A_{t} \right)} = \rho_{A} \log{\left(A_{t-1} \right)} + \epsilon_{A t}\]

\[\log{\left(G_{t} \right)} = \epsilon_{z t} + \log{\left(g_{z} \right)}\]

Shocks

\[\operatorname{Set}\left(\left[ \epsilon_{A t}, \ \epsilon_{z t}\right]\right)\]

Calibration

\[\rho_{A} = 0.95\]

\[g_{z} = 1.005\]

mod = ge.model_from_gcn(gcn_path, verbose=True)

Model Building Complete.

Found:

17 equations

17 variables

The following variables were eliminated at user request:

K_d_t, TC_t, U_t

The following "variables" were defined as constants and have been substituted away:

mc_t

6 stochastic shocks

0 / 6 have a defined prior.

14 parameters

13 / 14 have a defined prior.

0 parameters to calibrate.

17 / 17 variables have analytical steady-state values.

17 user-provided: A_ss, C_ss, G_ss, I_ss, K_ss, L_ss, R_f_ss,

Theta_ss, W_ss, Y_ss, beta_ss, lambda_ss,

q_ss, r_ss, shock_I_ss, shock_psi_ss, z_ss

Model appears well defined and ready to proceed to solving.

The Steady State#

The steady state is the long-run point around which the linearised model lives — the BGP values of every variable once trend growth has been factored out. Before we fit anything, it’s worth doing two sanity checks:

Inspect the steady state at the calibrated parameter values to make sure the numbers are economically sensible (positive consumption, \(r^{ss}\) in a plausible range, an investment-to-output ratio that matches what we’d expect for an advanced economy, etc.).

Propagate the prior uncertainty in the parameters to the steady state, so we can see what range of long-run worlds our prior actually contemplates. Each prior draw gives a different set of parameters; for each set we can solve the closed-form steady state in the

STEADY_STATEblock. The marginal distributions of the resulting steady-state values tell us whether the priors are tight enough to be informative, or whether they cover such a wide range that the data will have to do all the work.

At the initial calibration#

ss_init = mod.steady_state(verbose=False, progressbar=False)

pd.Series(dict(ss_init), name="value").round(4).to_frame()

| value | |

|---|---|

| A_ss | 1.0000 |

| C_ss | 1.7838 |

| G_ss | 1.0050 |

| I_ss | 0.5153 |

| K_ss | 17.2641 |

| L_ss | 0.9710 |

| R_f_ss | 0.0152 |

| Theta_ss | 1.0000 |

| W_ss | 1.6574 |

| Y_ss | 2.2991 |

| beta_ss | 0.9900 |

| lambda_ss | 0.5689 |

| q_ss | 0.5689 |

| r_ss | 0.0402 |

| shock_I_ss | 1.0000 |

| shock_psi_ss | 1.0000 |

| z_ss | 1.0000 |

A quick sanity scan:

\(r^{ss} \approx 0.040\) per quarter (\(\approx 16\%\) annualised) — high for modern Europe, driven by \(\beta = 0.99\) and \(\delta = 0.025\). Estimation will pull both of these.

\(L^{ss} \approx 0.97\) — close to one. With \(\Theta = 1\) and no scaling, the household supplies nearly all of its time; this is why the data needs the Hansen-style rescaling we’ll apply below.

\(i^{ss}/y^{ss} \approx 0.26\) and \(c^{ss}/y^{ss} \approx 0.74\) — standard RBC investment- and consumption-output ratios.

All shock states and the utilisation rate are exactly one at the BGP, by construction. The frictions vanish.

Under the prior#

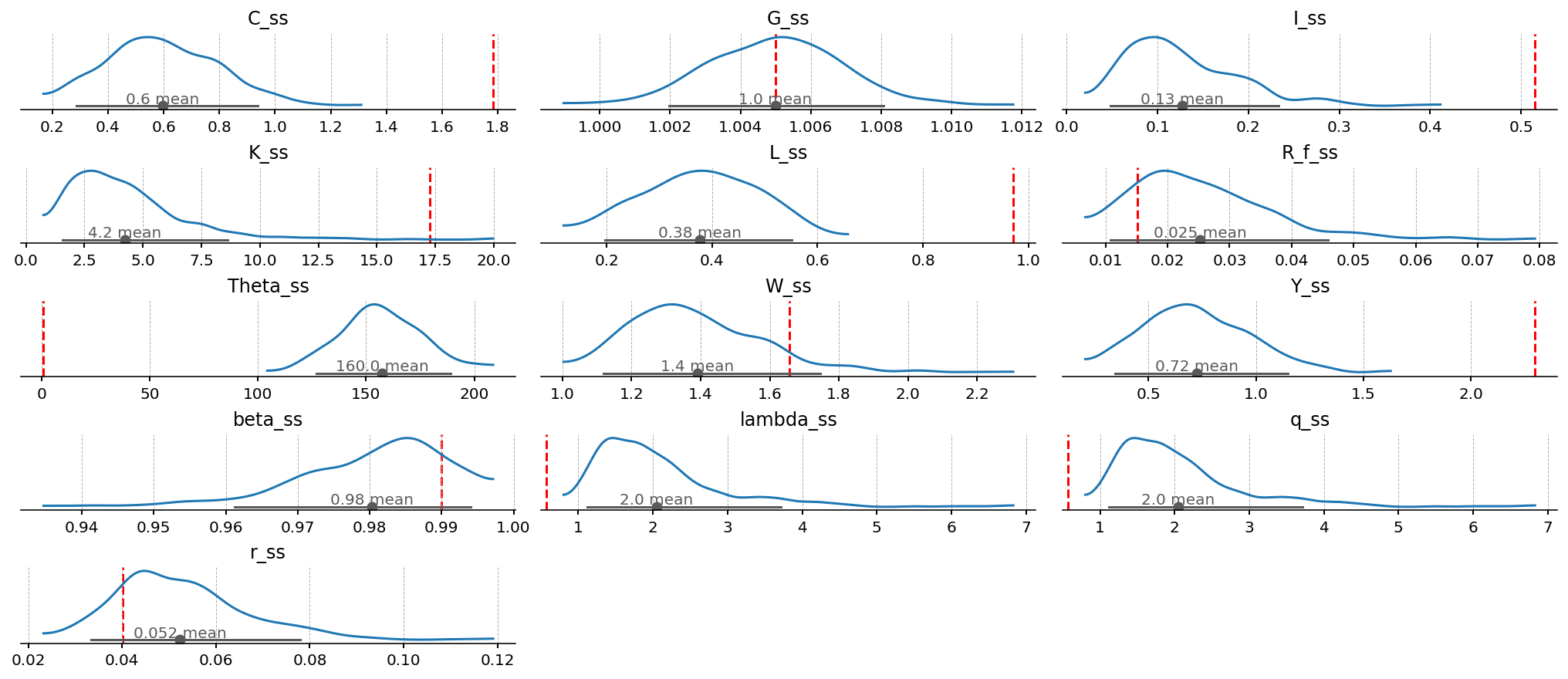

A single steady state is a single point. The priors define a whole distribution over plausible long-run worlds. We can visualise that distribution by sampling from the prior, evaluating the closed-form steady-state mapping at each draw, and looking at the marginal density of each steady-state quantity. Vertical lines mark the initial-calibration values.

ss_mod = ge.statespace_from_gcn(gcn_path, not_loglin_variables=["R_f"])

Model Building Complete.

Found:

17 equations

17 variables

The following variables were eliminated at user request:

K_d_t, TC_t, U_t

The following "variables" were defined as constants and have been substituted away:

mc_t

6 stochastic shocks

0 / 6 have a defined prior.

14 parameters

13 / 14 have a defined prior.

0 parameters to calibrate.

17 / 17 variables have analytical steady-state values.

17 user-provided: A_ss, C_ss, G_ss, I_ss, K_ss, L_ss, R_f_ss,

Theta_ss, W_ss, Y_ss, beta_ss, lambda_ss,

q_ss, r_ss, shock_I_ss, shock_psi_ss, z_ss

Model appears well defined and ready to proceed to solving.

Statespace model construction complete, but call the .configure method to finalize.

from pytensor.graph.replace import graph_replace

prior_dict = ss_mod.param_priors.copy()

with pm.Model(coords=ss_mod.coords) as m:

ss_mod.to_pymc()

# Tight Normal centred on the Theta implied by the observed labour mean:

# Theta ~ 157 gives L_ss = exp(mean(log_L)) ~ 0.18.

d = pz.Normal(mu=157.0, sigma=20.0)

prior_dict["Theta"] = d

d.to_pymc("Theta")

replacement_dict = {var: m[name] for name, var in ss_mod._name_to_variable.items() if name in m.named_vars}

for key, value in ss_mod.steady_state_mapping.items():

pm.Deterministic(key.name, graph_replace(value, replacement_dict, strict=False))

prior_idata = pm.sample_prior_predictive(random_seed=RANDOM_SEED)

deterministic_ss = ["A_ss", "shock_I_ss", "shock_psi_ss", "z_ss"]

ss_prior = prior_idata.prior.to_dataset()[list(mod.steady_state().keys())]

Sampling: [Theta, alpha, beta, delta, g_z, gamma_I, phi_H, psi_z, rho_A, rho_I, rho_Theta, rho_beta, rho_psi, sigma_L]

ss_prior_df = az.summary(ss_prior, var_names=[f"~{x}" for x in deterministic_ss]).drop(columns=["r_hat"])

ss_prior_df

| mean | sd | eti89_lb | eti89_ub | ess_bulk | ess_tail | mcse_mean | mcse_sd | |

|---|---|---|---|---|---|---|---|---|

| C_ss | 0.6 | 0.2 | 0.29 | 0.94 | 522 | 483 | 0.0086 | 0.0058 |

| G_ss | 1.005 | 0.002 | 1 | 1 | 621 | 466 | 7.9e-05 | 6e-05 |

| I_ss | 0.127 | 0.063 | 0.048 | 0.23 | 537 | 462 | 0.0027 | 0.0025 |

| K_ss | 4.2 | 2.5 | 1.6 | 8.6 | 497 | 433 | 0.12 | 0.16 |

| L_ss | 0.377 | 0.112 | 0.2 | 0.55 | 542 | 485 | 0.0048 | 0.0028 |

| R_f_ss | 0.025 | 0.011 | 0.011 | 0.046 | 482 | 367 | 0.0005 | 0.0005 |

| Theta_ss | 157 | 19 | 130 | 190 | 511 | 504 | 0.86 | 0.58 |

| W_ss | 1.39 | 0.21 | 1.1 | 1.7 | 499 | 430 | 0.0093 | 0.0092 |

| Y_ss | 0.72 | 0.25 | 0.34 | 1.1 | 544 | 501 | 0.011 | 0.0078 |

| beta_ss | 0.9804 | 0.0105 | 0.96 | 0.99 | 492 | 354 | 0.00047 | 0.00044 |

| lambda_ss | 2.05 | 0.9 | 1.1 | 3.7 | 531 | 438 | 0.04 | 0.053 |

| q_ss | 2.05 | 0.9 | 1.1 | 3.7 | 531 | 438 | 0.04 | 0.053 |

| r_ss | 0.052 | 0.014 | 0.033 | 0.078 | 426 | 382 | 0.00067 | 0.00061 |

ss_to_plot = [n for n in ss_prior.data_vars if float(ss_prior[n].std()) > 1e-6]

ss_init_dict = {n: float(ss_init[n]) for n in ss_to_plot}

pc = azp.plot_dist(

ss_prior,

var_names=ss_to_plot,

col_wrap=3,

figure_kwargs={"figsize": (14, 6)},

)

azp.add_lines(pc, ss_init_dict, visuals={"ref_line": {"color": "red", "linestyle": "--"}})

pc.show()

A few observations the plots make obvious:

\(\Theta^{ss}\) vs \(L^{ss}\). The initial calibration sits in the lower tail of \(\Theta^{ss}\) and in the upper tail of \(L^{ss}\). That is not an accident — \(\Theta\) and \(L^{ss}\) are inversely related through the labour-supply FOC, so any prior draw that pushes \(\Theta\) up pulls \(L^{ss}\) down. Both initial values look extreme relative to the prior, which is the formal expression of the Hansen-rescaling argument from earlier: the data lives near \(L \approx 0.18\), so the prior is going to want a much heavier \(\Theta\) than the calibration starts with.

\(r^{ss}\). Initial value is on the low side of the prior — the prior contemplates

r_ssbetween 2% and 12% per quarter (annualised: 8% to 60%). Reality is closer to 1–3% annually, and we’ll let the estimation pullbetatoward 1 anddeltatoward small values to get there.\(G^{ss}\). Tight, symmetric, centred on \(g_z = 1.005\). The prior on trend growth is informative; the data will refine it but won’t overturn it.

\(\beta^{ss}\). The prior is heavily right-skewed by construction (

Betawith a lot of mass near \(0.99\)), so the initial value \(0.99\) is at the upper tail.

Together this is a fine prior to take to the data: tight enough to rule out absurd long-run worlds (negative consumption, \(L^{ss} > 1\) that would mean working more than a full day), wide enough that the data has somewhere to move us.

French Data from Eurostat#

Eurostat publishes quarterly French national accounts (real GDP and its expenditure components in chain-linked 2015 euros) as well as quarterly labour-input data measured in hours actually worked. That is exactly what the model wants: \(L_t\) in the GCN is a labour input that, dimensionally, is hours per period, so we can build a clean hours-per-capita series directly.

The eurostat package wraps Eurostat’s SDMX REST API. Each dataset is identified by a short code (e.g. namq_10_gdp for national-accounts main aggregates), and we filter it by the dimensions that appear in the metadata: geography, seasonal adjustment, unit, accounting item, NACE branch, etc.

We pull:

Symbol |

Eurostat dataset |

Filter / interpretation |

|---|---|---|

\(Y\) |

|

Real GDP, chain-linked 2015 M€, SCA |

\(C\) |

|

Real household + NPISH final consumption, chain-linked 2015 M€, SCA |

\(I\) |

|

Real gross fixed capital formation, chain-linked 2015 M€, SCA |

|

|

Total hours worked, thousand hours, SCA |

\(N\) |

|

Working-age population 15–64, thousand persons |

|

|

Compensation of employees, nominal M€, SA |

\(P\) |

|

GDP deflator, index 2015 = 100, SCA |

|

|

10-year French government bond yield, annualised percent |

Derived series:

\(L\) expresses total hours worked as a fraction of the \(16\) waking hours per day per working-age person (the convention from Hansen 1985 — people have to sleep), which puts it on the same dimensionless \([0, 1]\) scale as the model’s \(L^{ss}\). Days per quarter are computed exactly so leap-year drift (Q1 has 90 vs 91 days) does not leak into the labour series.

The real wage is nominal compensation per hour worked, deflated by the GDP deflator at 2015 prices.

The quarterly real rate from Fisher: annualised 10-year yield converted to quarterly, deflated by quarterly inflation from the GDP deflator.

from pathlib import Path

import eurostat as es

def es_series(dataset, name, **filters):

"""Pull a single Eurostat time series and return a named ``pd.Series``.

``filters`` are passed straight through to ``eurostat.get_data_df`` as the

``filter_pars`` dictionary (each value is wrapped in a one-element list so

you can write ``geo="FR"`` instead of ``geo=["FR"]``). The dataset must

have its time dimension on columns named like ``"YYYY-Qn"``.

"""

df = es.get_data_df(dataset, filter_pars={k: [v] for k, v in filters.items()})

if len(df) != 1:

raise ValueError(f"{dataset} returned {len(df)} rows for {name}; tighten filters: {filters}")

time_cols = [c for c in df.columns if isinstance(c, str) and "-Q" in c]

s = pd.to_numeric(df[time_cols].iloc[0], errors="coerce")

s.index = pd.PeriodIndex(s.index, freq="Q").to_timestamp()

s.name = name

return s

cache_path = Path("fr_eurostat_data.csv")

required = ["Y", "C", "I", "L_hours", "N", "D1", "P", "i_nom"]

need_refresh = True

if cache_path.exists():

data = pd.read_csv(cache_path, index_col=0, parse_dates=[0])

need_refresh = not set(required).issubset(data.columns)

if need_refresh:

data = pd.concat(

[

es_series("namq_10_gdp", "Y", geo="FR", s_adj="SCA", unit="CLV15_MEUR", na_item="B1GQ"),

es_series("namq_10_gdp", "C", geo="FR", s_adj="SCA", unit="CLV15_MEUR", na_item="P31_S14_S15"),

es_series("namq_10_gdp", "I", geo="FR", s_adj="SCA", unit="CLV15_MEUR", na_item="P51G"),

es_series(

"namq_10_a10_e", "L_hours", geo="FR", s_adj="SCA", nace_r2="TOTAL", na_item="EMP_DC", unit="THS_HW"

),

es_series("namq_10_a10", "D1", geo="FR", s_adj="SA", nace_r2="TOTAL", na_item="D1", unit="CP_MEUR"),

es_series("namq_10_gdp", "P", geo="FR", s_adj="SCA", unit="PD15_EUR", na_item="B1GQ"),

es_series(

"lfsq_pganws", "N", geo="FR", age="Y15-64", sex="T", citizen="TOTAL", wstatus="POP", unit="THS_PER"

),

es_series("irt_lt_mcby_q", "i_nom", geo="FR", int_rt="MCBY"),

],

axis=1,

)

data.index.name = "Time"

data.to_csv(cache_path)

data.tail()

| Y | C | I | L_hours | D1 | P | N | i_nom | |

|---|---|---|---|---|---|---|---|---|

| Time | ||||||||

| 2025-01-01 | 615341.9 | 329412.8 | 133012.2 | 11555800.0 | 381012.9 | 120.120 | 41354.5 | 3.30500 |

| 2025-04-01 | 617501.9 | 329332.3 | 133526.0 | 11543600.0 | 382597.8 | 120.174 | 41371.6 | 3.25341 |

| 2025-07-01 | 620923.5 | 329660.8 | 134567.3 | 11550900.0 | 384013.7 | 120.565 | 41392.8 | 3.43000 |

| 2025-10-01 | 622228.7 | 330832.7 | 134988.3 | 11542600.0 | 386328.9 | 121.106 | 41414.4 | 3.44000 |

| 2026-01-01 | 622197.9 | 330450.4 | 134487.8 | NaN | NaN | NaN | NaN | 3.52744 |

Raw coverage:

Y 1980-01-01 -> 2026-01-01 (185 obs)

C 1980-01-01 -> 2026-01-01 (185 obs)

I 1980-01-01 -> 2026-01-01 (185 obs)

L_hours 1980-01-01 -> 2025-10-01 (184 obs)

D1 1980-01-01 -> 2025-10-01 (184 obs)

P 1980-01-01 -> 2025-10-01 (184 obs)

N 1998-01-01 -> 2025-10-01 (97 obs)

i_nom 1980-01-01 -> 2026-01-01 (185 obs)

df = pd.DataFrame(index=data.index)

df["Y"] = data["Y"]

df["C"] = data["C"]

df["I"] = data["I"]

ACTIVE_HOURS_PER_DAY = 16

period = data.index.to_period("Q")

days_in_quarter = (period.asfreq("D", "end").to_timestamp() - period.asfreq("D", "start").to_timestamp()).days + 1

df["L"] = data["L_hours"] / data["N"] / (ACTIVE_HOURS_PER_DAY * days_in_quarter)

# Real wage: nominal compensation per hour, deflated by the GDP deflator

# (base 2015 = 100).

df["w"] = (data["D1"] / data["L_hours"]) / (data["P"] / 100.0)

# Quarterly real rate from Fisher: annualised 10y yield -> quarterly, deflated

# by quarterly inflation from the GDP deflator.

pi_q = data["P"].pct_change()

i_q = (1.0 + data["i_nom"] / 100.0) ** 0.25 - 1.0

df["r"] = (1.0 + i_q) / (1.0 + pi_q) - 1.0

df = df[["Y", "C", "I", "L", "w", "r"]].dropna(how="all")

df.index.freq = "QS"

df.tail()

| Y | C | I | L | w | r | |

|---|---|---|---|---|---|---|

| Time | ||||||

| 2025-01-01 | 615341.9 | 329412.8 | 133012.2 | 0.194050 | 0.027449 | 0.004561 |

| 2025-04-01 | 617501.9 | 329332.3 | 133526.0 | 0.191636 | 0.027580 | 0.007583 |

| 2025-07-01 | 620923.5 | 329660.8 | 134567.3 | 0.189576 | 0.027575 | 0.005196 |

| 2025-10-01 | 622228.7 | 330832.7 | 134988.3 | 0.189341 | 0.027637 | 0.003986 |

| 2026-01-01 | 622197.9 | 330450.4 | 134487.8 | NaN | NaN | NaN |

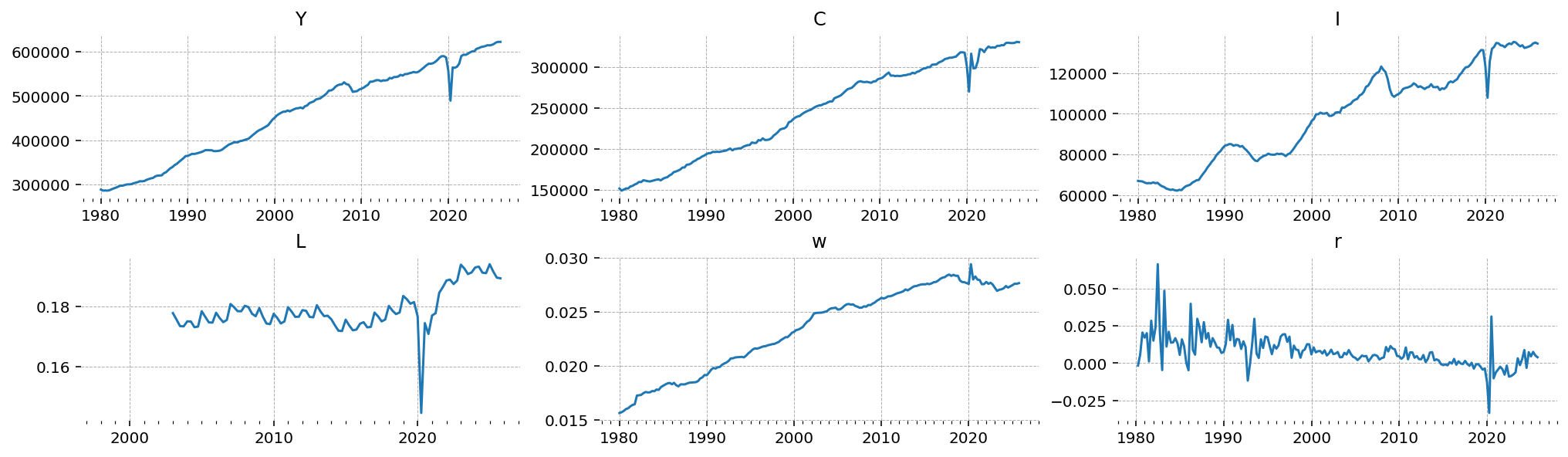

Raw series#

The six series, untouched. The big picture: \(Y\), \(C\), \(I\), and \(w\) trend strongly upwards (they inherit the unit root in productivity); \(L\) and \(r\) look stationary.

gp.plot_timeseries(df, n_cols=3, fig_kwargs={"figsize": (14, 4)});

Preprocessing for the Kalman filter#

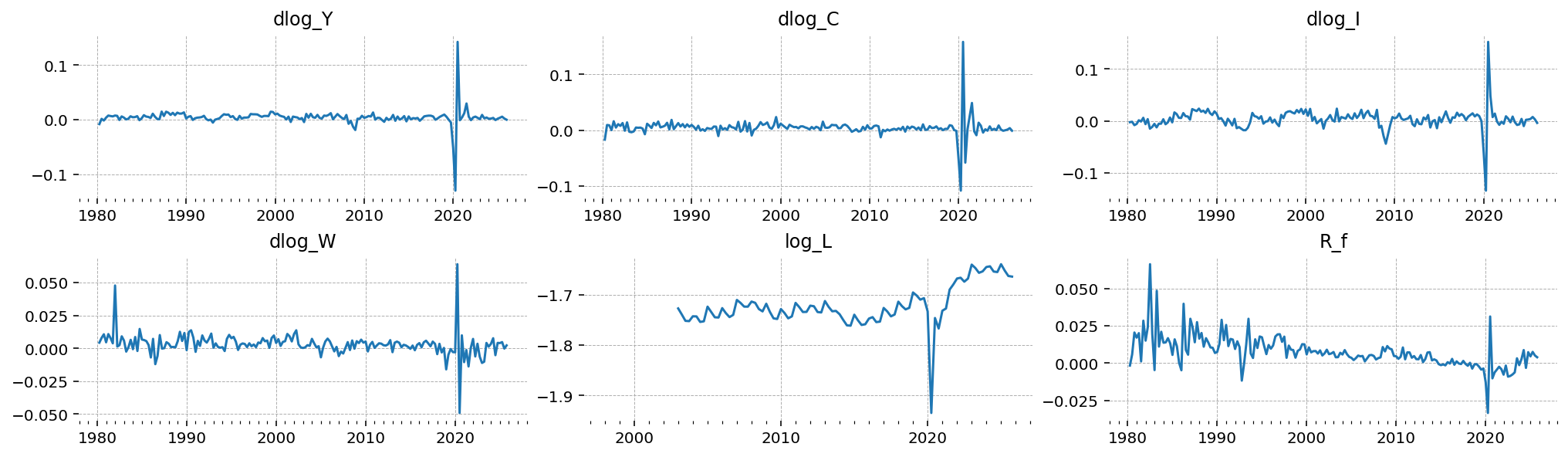

The linearized model has stationary states — \(\hat y_t\), \(\hat c_t\), \(\hat L_t\), etc., all in log-deviations from steady state — and we need to feed it stationary observables. Two transformations cover all six series:

Trending real-side variables (\(Y\), \(C\), \(I\), \(w\)). These inherit the unit root in \(Z_t\), so we take the first difference of the log to convert them into quarterly real growth rates. In the model, \(\Delta \log Y_t = \log G_t + \Delta \hat{y}_t\), and because \(\log G_t\) has long-run mean \(\log g_z\), the long-run mean of each transformed series is the single model parameter \(\log g_z\).

Naturally stationary variables (\(L\), \(r\)). \(L\) is hours per working-age person; we log it. \(r\) is already a quarterly real rate, so we leave it on the decimal scale. Their long-run means are \(\log L^{ss}\) and \(r^{ss}\) respectively.

Critically, we do not subtract sample means or fit a deterministic trend. gEconpy supports putting the model’s steady state directly into the observation-equation intercepts — so for every observable, the mean of the data lines up against a single model number (\(\log g_z\), \(\log L^{ss}\), or \(r^{ss}\)). The estimation procedure then treats deviations from those steady-state means as informative about the structural parameters, instead of throwing them away in a preprocessing step.

df_obs = pd.DataFrame(index=df.index)

# Trending real-side variables: log + first difference -> quarterly real growth rates.

# Column names encode the transformation (`dlog_X`) and are deliberately distinct

# from the latent-state names (Y, C, I, W) that appear in the GCN.

for col, name in [("Y", "dlog_Y"), ("C", "dlog_C"), ("I", "dlog_I"), ("w", "dlog_W")]:

df_obs[name] = np.log(df[col]).diff()

# Stationary variables. log_L is observed in logs; the real interest rate maps

# onto the model's net risk-free rate R_f (a level, not a log).

df_obs["log_L"] = np.log(df["L"])

df_obs["R_f"] = df["r"]

df_obs = df_obs.dropna(how="all")

df_obs.describe()

| dlog_Y | dlog_C | dlog_I | dlog_W | log_L | R_f | |

|---|---|---|---|---|---|---|

| count | 184.000000 | 184.000000 | 184.000000 | 183.000000 | 97.000000 | 183.000000 |

| mean | 0.004174 | 0.004232 | 0.003785 | 0.003108 | -1.721223 | 0.007613 |

| std | 0.015697 | 0.016851 | 0.019370 | 0.008499 | 0.039445 | 0.010591 |

| min | -0.129838 | -0.108797 | -0.134123 | -0.049190 | -1.934368 | -0.033394 |

| 25% | 0.001593 | 0.000756 | -0.002873 | 0.000461 | -1.742982 | 0.001986 |

| 50% | 0.004425 | 0.004226 | 0.004512 | 0.003426 | -1.728491 | 0.006082 |

| 75% | 0.007129 | 0.007909 | 0.011448 | 0.005755 | -1.709883 | 0.011844 |

| max | 0.142350 | 0.158507 | 0.152297 | 0.064056 | -1.639637 | 0.066406 |

gp.plot_timeseries(df_obs, n_cols=3, fig_kwargs={"figsize": (14, 4)});

Masking the COVID-19 quarters#

The six panels above share a feature that will wreck the estimation if we ignore it: the 2020 spikes. French real GDP fell 13.5% in 2020 Q2 and rebounded 18.5% in Q3 — and consumption, investment, hours, and the wage all moved with it. In the transformed dlog_* series these quarters are 6-to-9-standard-deviation events relative to the rest of the sample.

A Gaussian Kalman filter has no way to treat such observations as the rare draws they are. Its likelihood penalises a prediction error quadratically, so a 9\(\sigma\) quarter contributes on the order of \(-40\) to the log-likelihood — by itself larger than the entire contribution of a normal decade. The estimator will do whatever it takes to soften that, and the cheapest lever available is the measurement-error variance: inflating error_sigma for an observable turns its COVID prediction error from “9\(\sigma\)” into “3\(\sigma\) of a much larger \(\sigma\)”. But measurement error is a single scalar, constant over time — buying that relief in 2020 means carrying an oversized error variance across all ~180 normal quarters too. The series most exposed to this ends up explained as almost pure noise, and the structural parameters that shape it (here, the consumption-habit parameter \(\phi_H\)) stop being disciplined by data: their posteriors are then pinned by the prior and the cross-equation restrictions, not by the business-cycle dynamics they are supposed to describe.

One way to deal with this is to treat the COVID quarters as missing. The Kalman filter handles missing observations natively — it runs the prediction step but skips the measurement update, so those quarters contribute nothing to the likelihood and the latent states over the gap are reconstructed from the model’s transition dynamics alone. We mask 2020 Q1 through 2021 Q1: the crash, the rebound, the second-lockdown dip, and the still-distorted early recovery.

# Mask the COVID crash, rebound, and early recovery: NaN rows are skipped in

# the Kalman measurement update.

covid_quarters = pd.period_range("2020Q1", "2021Q3", freq="Q").to_timestamp()

df_obs_masked = df_obs.copy()

df_obs_masked.loc[df_obs.index.isin(covid_quarters)] = np.nan

print(f"Masked {len(covid_quarters)} quarters: {covid_quarters.min().date()} -> {covid_quarters.max().date()}")

df_obs_masked.loc["2019-10-01":"2021-07-01"]

Masked 7 quarters: 2020-01-01 -> 2021-07-01

| dlog_Y | dlog_C | dlog_I | dlog_W | log_L | R_f | |

|---|---|---|---|---|---|---|

| Time | ||||||

| 2019-10-01 | -0.005059 | -0.00154 | -0.000271 | -0.002846 | -1.706902 | -0.003547 |

| 2020-01-01 | NaN | NaN | NaN | NaN | NaN | NaN |

| 2020-04-01 | NaN | NaN | NaN | NaN | NaN | NaN |

| 2020-07-01 | NaN | NaN | NaN | NaN | NaN | NaN |

| 2020-10-01 | NaN | NaN | NaN | NaN | NaN | NaN |

| 2021-01-01 | NaN | NaN | NaN | NaN | NaN | NaN |

| 2021-04-01 | NaN | NaN | NaN | NaN | NaN | NaN |

| 2021-07-01 | NaN | NaN | NaN | NaN | NaN | NaN |

gp.plot_timeseries(df_obs_masked, n_cols=3, fig_kwargs={"figsize": (14, 4)});

Fitting the Model#

Estimation is a three-step routine: configure the state space, build the PyMC graph, then sample. We start with ss_mod.configure(...), which freezes the structural choices the Kalman filter needs.

The two interesting options for our setup are observation_equations and ss_obs_intercept.

observation_equations is a dictionary mapping the name of an observed series (the LHS) to a GCN-style string expressing the observation in terms of latent model variables and parameters (the RHS). The LHS can be a brand-new name — it does not have to match any latent state. For the trending real-side variables we observe quarterly real growth rates, which the model writes as the log change in \(X_t \cdot Z_t / Z_{t-1}\):

and similarly for \(C\), \(I\), \(W\). For \(L\) we observe the log of the stationary level. The state-space machinery parses each equation, linearises it around the steady state, and produces both the design-matrix row and the constant (intercept) term automatically — so the BGP growth rate \(\log g_z\) ends up baked into the intercepts of the four dlog_* observables, and \(\log L^{ss}\) becomes the intercept of log_L. No demeaning required.

ss_obs_intercept is a list of observed-state names that don’t get an explicit observation equation — they’re observed directly off a latent state, and we want the Kalman filter to use that state’s steady-state value as the intercept. The real interest rate r is the only example here: the model latent r[] IS the observation (in level), and we want the intercept to be \(r^{ss}\) on every parameter draw.

observation_equations = {

"dlog_Y": "log(Y[] / Y[-1] * G[])",

"dlog_C": "log(C[] / C[-1] * G[])",

"dlog_I": "log(I[] / I[-1] * G[])",

"dlog_W": "log(W[] / W[-1] * G[])",

"log_L": "log(L[])",

}

# R_f has no observation equation: it is observed directly off the latent

# state, with the steady-state value used as the observation intercept.

ss_mod.configure(

observed_states=list(df_obs.columns),

observation_equations=observation_equations,

ss_obs_intercept=["R_f"],

measurement_error=list(df_obs.columns),

mode="JAX",

solver="scan_cycle_reduction",

max_iter=13,

use_adjoint_gradients=True,

use_direct_lyapunov=False,

)

Model Requirements Variable Shape Constraints Dimensions ──────────────────────────────────────────────────────── Theta () None alpha () None beta () None delta () None g_z () None gamma_I () None phi_H () None psi_z () None rho_A () None rho_I () None rho_Theta () None rho_beta () None rho_psi () None sigma_L () None sigma_epsilon_A () Positive None sigma_epsilon_I () Positive None sigma_epsilon_Theta () Positive None sigma_epsilon_beta () Positive None sigma_epsilon_psi () Positive None sigma_epsilon_z () Positive None error_sigma_dlog_Y () Positive None error_sigma_dlog_C () Positive None error_sigma_dlog_I () Positive None error_sigma_dlog_W () Positive None error_sigma_log_L () Positive None error_sigma_R_f () Positive None These parameters should be assigned priors inside a PyMC model block before calling the build_statespace_graph method.

Building the PyMC graph#

Every parameter listed by configure() needs to live as a PyMC random variable before we can call build_statespace_graph. The 14 structural parameters already have priors from the GCN, so ss_mod.to_pymc() registers them in one call. The remaining twelve standard-deviations (six structural shocks, six measurement errors) are not in the GCN by design — they’re estimation-time choices — so we set them by hand.

The data is in growth-rate / log-level scale, so both kinds of \(\sigma\) live somewhere around the 0.001–0.05 band; a maxent(Gamma, lower=0.001, upper=0.05) prior pins 99% of the prior mass inside that range.

with pm.Model(coords=ss_mod.coords) as rbc_growth_pm:

ss_mod.to_pymc()

prior_dict = ss_mod.param_priors.copy()

# Theta sets the steady-state level of labour and has no GCN prior. It is

# only weakly identified: L_ss is a joint function of Theta, sigma_L and

# alpha, so a loose prior leaves a ridge the sampler cannot traverse. Pin

# it with a tight Normal centred on the value implied by the observed

# labour mean -- Theta ~ 157 gives L_ss = exp(mean(log_L)) ~ 0.18.

d = pz.Normal(mu=157.0, sigma=10.0)

prior_dict["Theta"] = d

d.to_pymc("Theta")

for shock in ss_mod.shock_names:

d = pz.maxent(pz.Gamma(), lower=0.001, upper=0.05, plot=False)

prior_dict[f"sigma_{shock}"] = d

d.to_pymc(f"sigma_{shock}")

for obs in ss_mod.error_states:

d = pz.maxent(pz.Gamma(), lower=0.001, upper=0.05, plot=False)

prior_dict[f"error_sigma_{obs}"] = d

d.to_pymc(f"error_sigma_{obs}")

ss_mod.build_statespace_graph(

data=df_obs_masked[list(ss_mod.observed_states)],

)

/Users/jessegrabowski/mambaforge/envs/geconpy-dev/lib/python3.12/site-packages/pymc_extras/statespace/utils/data_tools.py:179: ImputationWarning: Provided data contains missing values and will be automatically imputed as hidden states during Kalman filtering.

warnings.warn(impute_message, ImputationWarning)

import nutpie as ntp

initial_points = {k: v + 1e-7 for k, v in ss_mod.param_dict.items() if k in [x.name for x in rbc_growth_pm.basic_RVs]}

initial_points["Theta"] = 100.0

ntp_mod = ntp.compile_pymc_model(

rbc_growth_pm,

backend="jax",

gradient_backend="jax",

freeze_model=True,

default_initialization_strategy="prior",

jitter_rvs=None,

initial_points=initial_points,

)

from jax import nn

idata = ntp.sample(

(

ntp_mod.with_transform_adapt(

verbose=False,

show_progress=False,

activation=nn.swish,

)

),

tune=2000,

draws=500,

chains=4,

adaptation="flow",

)

Sampler Progress

Total Chains: 4

Active Chains: 0

Finished Chains: 4

Sampling for 7 minutes

Estimated Time to Completion: now

| Progress | Draws | Divergences | Step Size | Gradients/Draw |

|---|---|---|---|---|

| 2500 | 0 | 0.65 | 7 | |

| 2500 | 0 | 0.69 | 7 | |

| 2500 | 0 | 0.69 | 7 | |

| 2500 | 0 | 0.69 | 7 |

Posterior Diagnostics#

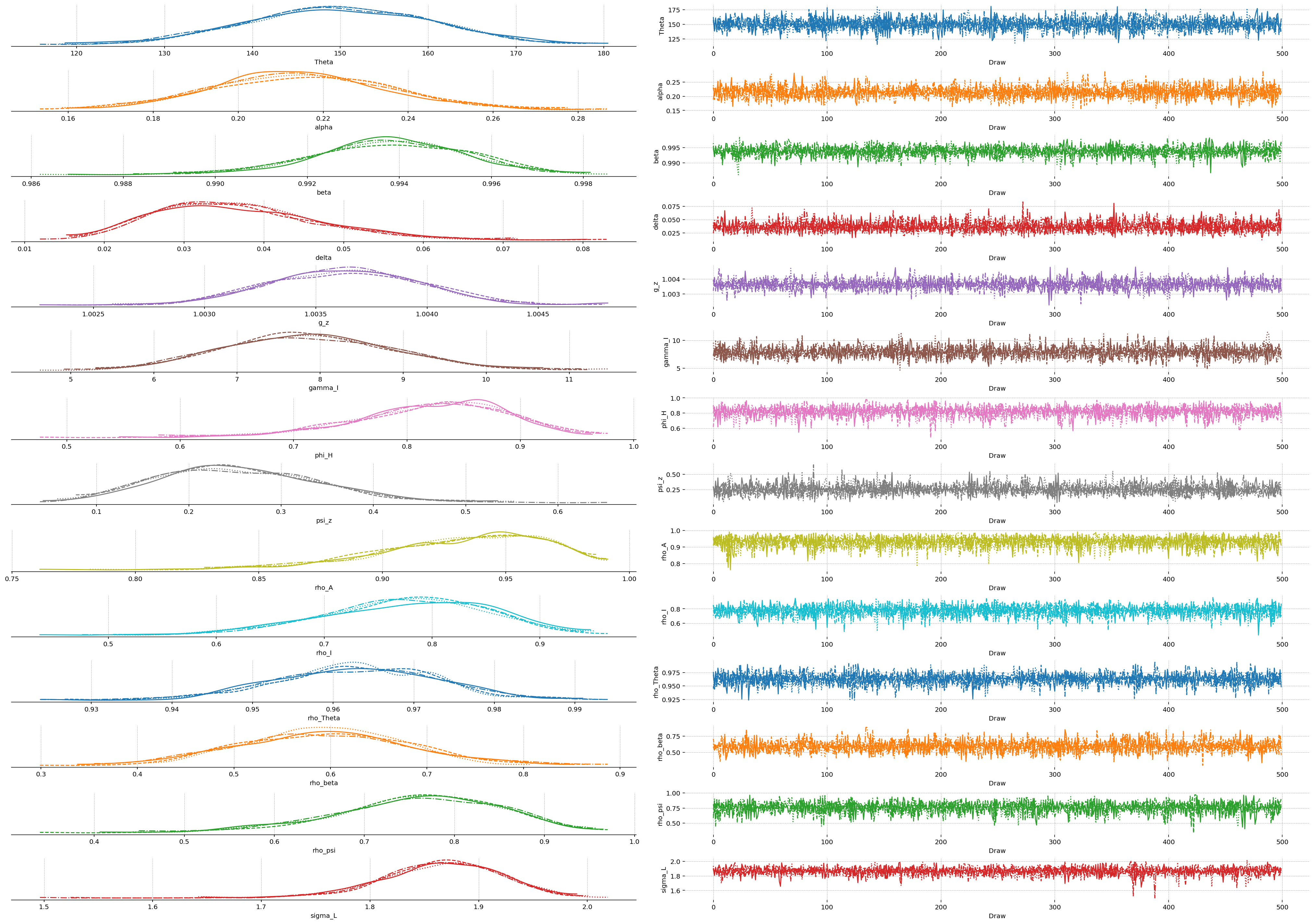

Once sampling finishes, the first stop is convergence: have the chains mixed, have they explored the posterior, and is the effective sample size large enough to take the summary numbers seriously? For a six-shock DSGE with 26 estimated parameters, trace plots and az.summary are the minimum sanity check.

We split the parameter list into three logical groups: the structural / deep parameters (the 14 entries with GCN priors), the shock standard deviations (sigma_epsilon_*), and the measurement-error standard deviations (error_sigma_*). Posterior shapes for each group tell different stories, so it pays to look at them separately.

deep_params = list(ss_mod.param_dict.keys())

shock_sigmas = [f"sigma_{s}" for s in ss_mod.shock_names]

error_sigmas = [f"error_sigma_{s}" for s in ss_mod.error_states]

az.summary(idata, var_names=deep_params + shock_sigmas + error_sigmas, round_to=3)

| mean | sd | eti89_lb | eti89_ub | ess_bulk | ess_tail | r_hat | mcse_mean | mcse_sd | |

|---|---|---|---|---|---|---|---|---|---|

| Theta | 149.908 | 10.207 | 133.412 | 166.172 | 5894.716 | 1588.999 | 1.004 | 0.133 | 0.089 |

| alpha | 0.215 | 0.021 | 0.183 | 0.249 | 4678.697 | 1391.190 | 1.004 | 0.000 | 0.000 |

| beta | 0.994 | 0.002 | 0.991 | 0.996 | 4113.808 | 1589.237 | 1.001 | 0.000 | 0.000 |

| delta | 0.037 | 0.010 | 0.023 | 0.054 | 4665.378 | 1653.002 | 1.005 | 0.000 | 0.000 |

| g_z | 1.004 | 0.000 | 1.003 | 1.004 | 6545.150 | 1672.232 | 1.005 | 0.000 | 0.000 |

| gamma_I | 7.887 | 1.031 | 6.312 | 9.563 | 5049.032 | 1624.744 | 1.004 | 0.015 | 0.011 |

| phi_H | 0.821 | 0.070 | 0.701 | 0.918 | 4542.009 | 1587.434 | 1.000 | 0.001 | 0.001 |

| psi_z | 0.255 | 0.088 | 0.126 | 0.401 | 4113.406 | 1419.538 | 1.000 | 0.001 | 0.001 |

| rho_A | 0.931 | 0.035 | 0.870 | 0.976 | 4303.360 | 1511.364 | 1.005 | 0.001 | 0.000 |

| rho_I | 0.775 | 0.077 | 0.643 | 0.886 | 4458.025 | 1771.862 | 1.004 | 0.001 | 0.001 |

| rho_Theta | 0.963 | 0.011 | 0.946 | 0.979 | 5820.256 | 1373.250 | 1.008 | 0.000 | 0.000 |

| rho_beta | 0.595 | 0.087 | 0.461 | 0.732 | 3547.959 | 1528.331 | 1.007 | 0.001 | 0.001 |

| rho_psi | 0.759 | 0.092 | 0.595 | 0.892 | 5505.926 | 1358.054 | 1.005 | 0.001 | 0.001 |

| sigma_L | 1.866 | 0.055 | 1.774 | 1.946 | 4792.025 | 1502.964 | 1.001 | 0.001 | 0.001 |

| sigma_epsilon_A | 0.002 | 0.001 | 0.000 | 0.003 | 4600.018 | 1502.088 | 1.001 | 0.000 | 0.000 |

| sigma_epsilon_I | 0.011 | 0.002 | 0.007 | 0.015 | 4231.803 | 1677.051 | 1.002 | 0.000 | 0.000 |

| sigma_epsilon_Theta | 0.024 | 0.003 | 0.020 | 0.029 | 5033.407 | 1497.048 | 1.004 | 0.000 | 0.000 |

| sigma_epsilon_beta | 0.005 | 0.001 | 0.003 | 0.007 | 3588.853 | 1746.742 | 1.000 | 0.000 | 0.000 |

| sigma_epsilon_psi | 0.015 | 0.010 | 0.003 | 0.034 | 5285.584 | 1607.809 | 1.001 | 0.000 | 0.000 |

| sigma_epsilon_z | 0.004 | 0.001 | 0.003 | 0.005 | 3856.080 | 1553.218 | 1.002 | 0.000 | 0.000 |

| error_sigma_dlog_Y | 0.003 | 0.000 | 0.002 | 0.003 | 4398.187 | 1393.186 | 1.004 | 0.000 | 0.000 |

| error_sigma_dlog_C | 0.005 | 0.000 | 0.004 | 0.005 | 5222.385 | 1468.102 | 1.003 | 0.000 | 0.000 |

| error_sigma_dlog_I | 0.004 | 0.001 | 0.002 | 0.005 | 4749.154 | 1370.459 | 1.004 | 0.000 | 0.000 |

| error_sigma_dlog_W | 0.004 | 0.000 | 0.004 | 0.005 | 5861.110 | 1487.360 | 1.000 | 0.000 | 0.000 |

| error_sigma_log_L | 0.009 | 0.001 | 0.008 | 0.011 | 6602.060 | 1772.543 | 1.003 | 0.000 | 0.000 |

| error_sigma_R_f | 0.007 | 0.001 | 0.006 | 0.009 | 4546.410 | 1354.833 | 1.002 | 0.000 | 0.000 |

az.plot_trace_dist(idata, var_names=list(deep_params));

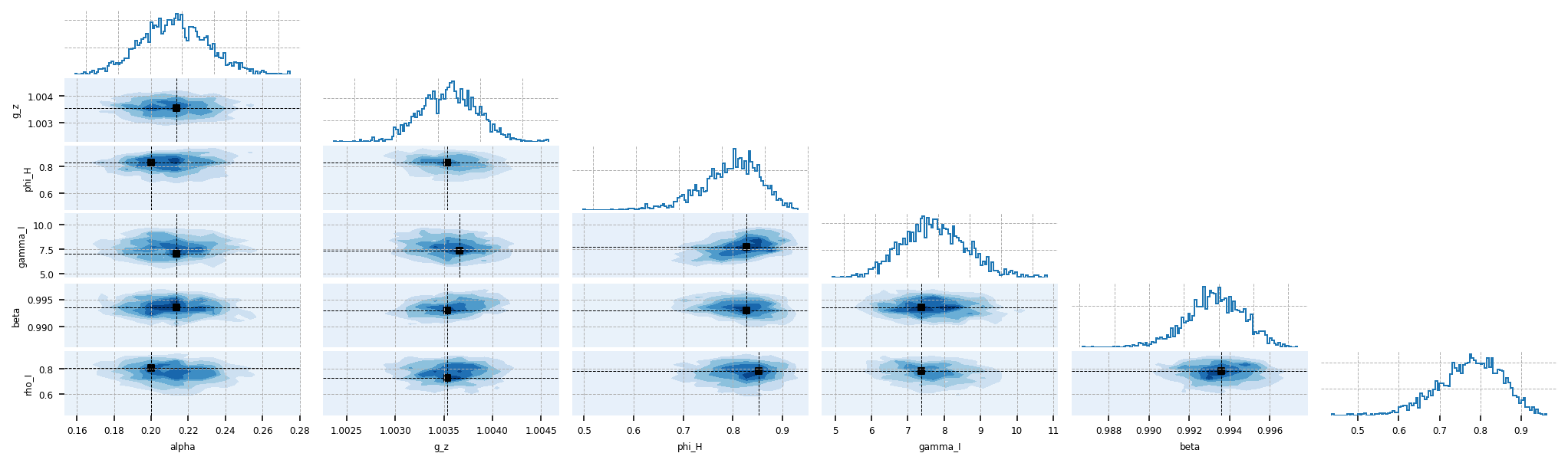

gp.plot_corner(idata, var_names=["alpha", "g_z", "phi_H", "gamma_I", "beta", "rho_I"]);

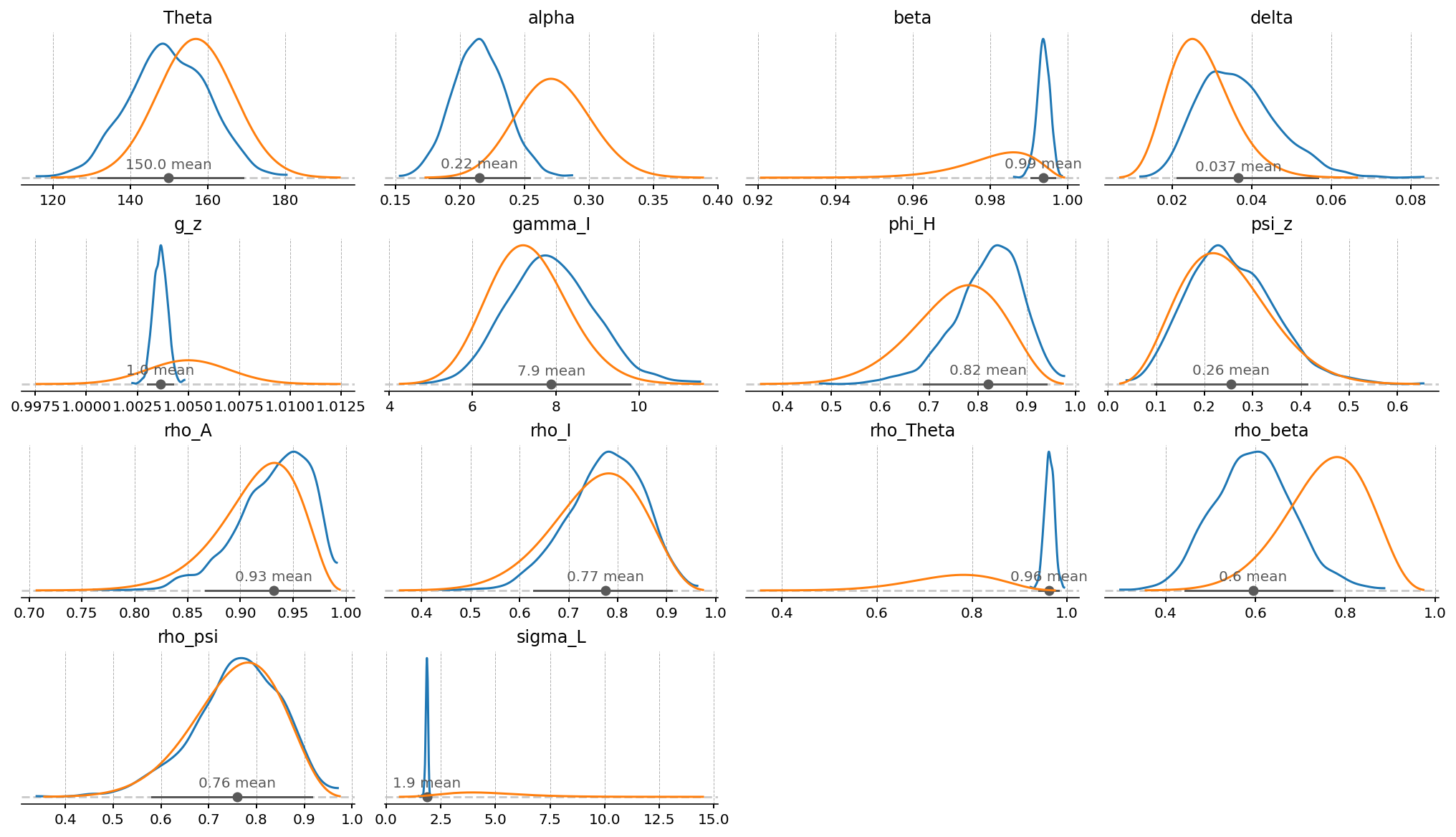

Posterior vs. prior#

The structural posteriors are most informative when overlaid on the priors that generated them. A posterior that hugs its prior means the data did not move the parameter (it is weakly identified); a posterior that is narrow and far from the prior mode means the data has a lot to say about it. We use the same prior_dict we built when configuring the PyMC model so the two distributions are plotted on a common scale.

gp.plot_posterior_with_prior(

idata, var_names=deep_params, prior_dict=prior_dict, n_cols=4, fig_kwargs={"figsize": (14, 8)}

);

/Users/jessegrabowski/mambaforge/envs/geconpy-dev/lib/python3.12/site-packages/pytensor_distributions/beta.py:106: FutureWarning: pytensor.tensor.xlogx.xlogy0 is deprecated. Use pytensor.tensor.special.xlogy(x, y) instead.

(xlogy0((alpha - 1), x) + xlogy0((beta - 1), 1 - x))

/Users/jessegrabowski/mambaforge/envs/geconpy-dev/lib/python3.12/site-packages/pytensor_distributions/beta.py:106: FutureWarning: pytensor.tensor.xlogx.xlogy0 is deprecated. Use pytensor.tensor.special.xlogy(x, y) instead.

(xlogy0((alpha - 1), x) + xlogy0((beta - 1), 1 - x))

/Users/jessegrabowski/mambaforge/envs/geconpy-dev/lib/python3.12/site-packages/pytensor_distributions/beta.py:107: FutureWarning: pytensor.tensor.xlogx.xlogy0 is deprecated. Use pytensor.tensor.special.xlogy(x, y) instead.

- (xlogy0((alpha + beta - 1), 1) + betaln(alpha, beta)),

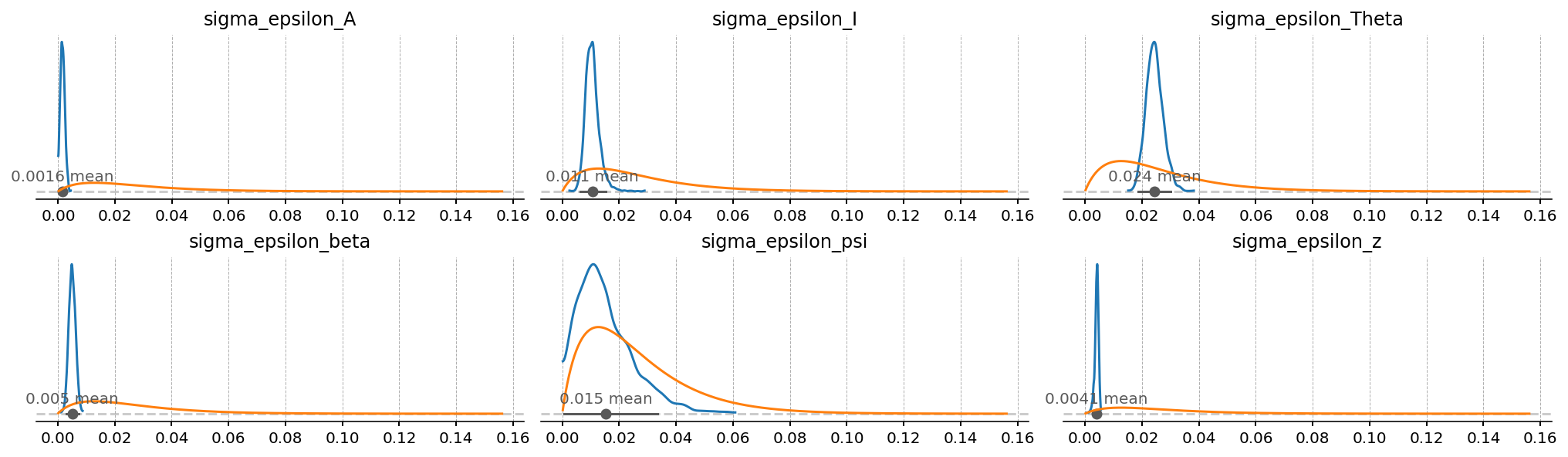

Shock and measurement-error scales#

The six \(\sigma_{\varepsilon,\cdot}\) tell us how big the structural innovations are. The six measurement-error \(\sigma\)s tell us, for each observable, how much the Kalman filter is allowed to attribute to “noise” rather than to model dynamics. Series with a large posterior measurement-error are series the model is having to give up on — the structure cannot reproduce them and the filter is reaching for white-noise slack instead.

gp.plot_posterior_with_prior(

idata, var_names=shock_sigmas, prior_dict=prior_dict, n_cols=3, fig_kwargs={"figsize": (14, 4)}

);

Smoothed Latent States#

The Kalman smoother infers the path of every latent state — the stationary cycle, the trend growth rate, the AR(1) shock processes — conditional on the entire observed sample and the posterior draws of the parameters. Two outputs are usually most informative:

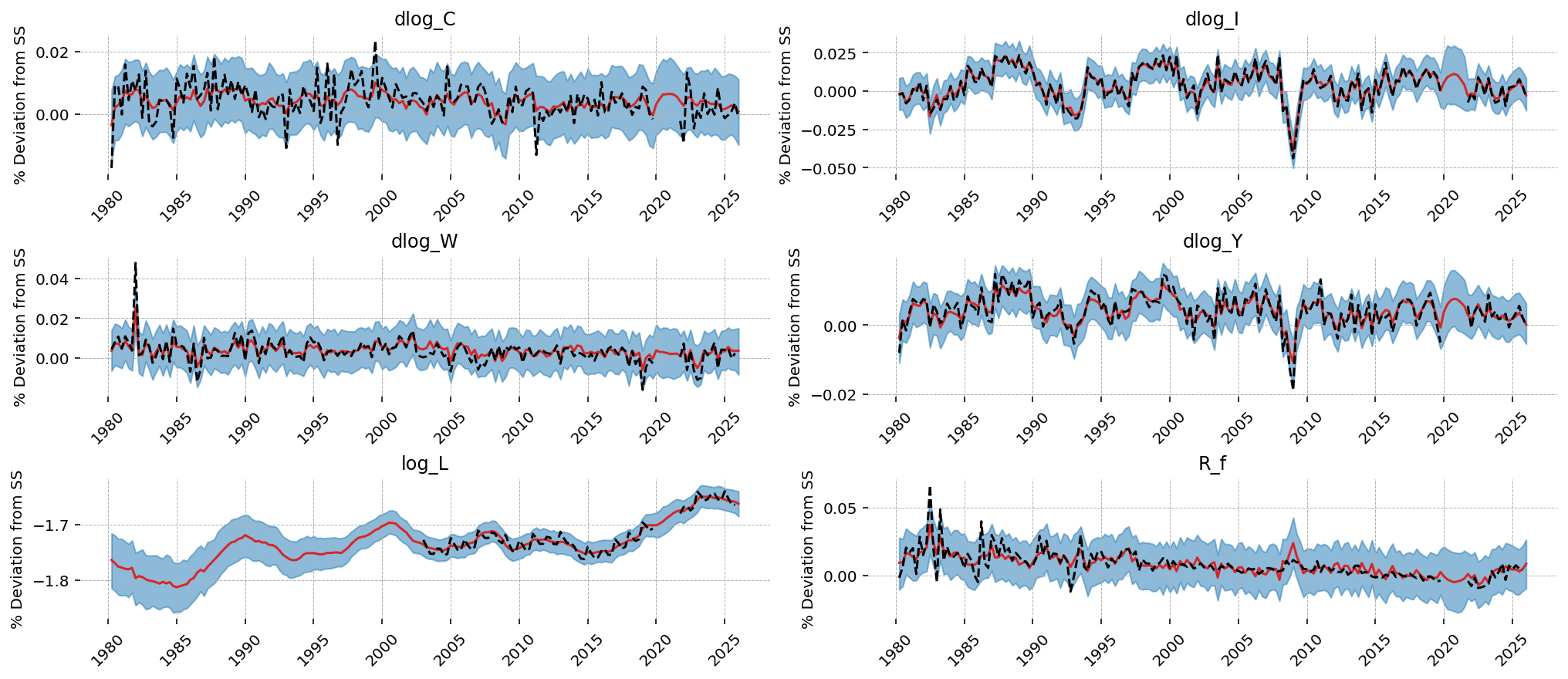

Smoothed observables. For each observed series, the model’s best guess of where the signal (data minus measurement error) actually was. Tight match means the model thinks it understood that series; loose match means it had to absorb structural mis-specification into measurement error.

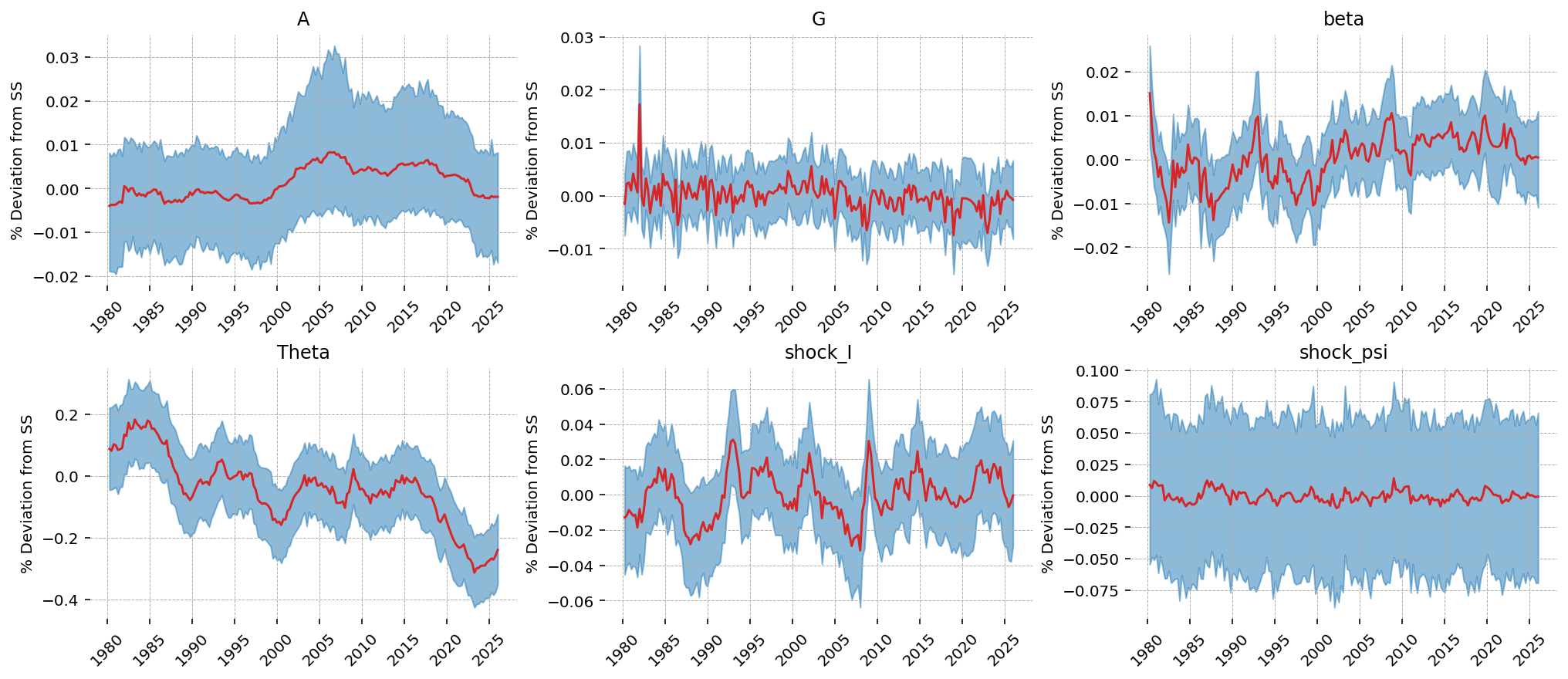

Smoothed latent shocks. The four taste / friction shock states (\(\beta_t\), \(\Theta_t\), \(\xi^I_t\), \(\xi^\psi_t\)) plus the two technology states (\(A_t\), \(G_t\)). These are the structural drivers the model attributes to every wiggle in the data.

ss_mod.sample_conditional_posterior runs the smoother on every posterior draw and stores the filtered, predicted, and smoothed paths back into an InferenceData. gp.plot_kalman_filter is the canonical visualisation.

latent_states = ss_mod.sample_conditional_posterior(idata, random_seed=rng, compile_kwargs={"mode": "NUMBA"})

/Users/jessegrabowski/mambaforge/envs/geconpy-dev/lib/python3.12/site-packages/pymc_extras/statespace/utils/data_tools.py:179: ImputationWarning: Provided data contains missing values and will be automatically imputed as hidden states during Kalman filtering.

warnings.warn(impute_message, ImputationWarning)

Sampling: [filtered_posterior, filtered_posterior_observed, predicted_posterior, predicted_posterior_observed, smoothed_posterior, smoothed_posterior_observed]

gp.plot_kalman_filter(

idata=latent_states,

data=df_obs_masked,

vars_to_plot=["dlog_C", "dlog_I", "dlog_W", "dlog_Y", "log_L", "R_f"],

kalman_output="smoothed",

n_cols=2,

figsize=(14, 6),

observed=True,

);

gp.plot_kalman_filter(

idata=latent_states,

data=df_obs,

kalman_output="smoothed",

vars_to_plot=["A", "G", "beta", "Theta", "shock_I", "shock_psi"],

n_cols=3,

figsize=(14, 6),

);

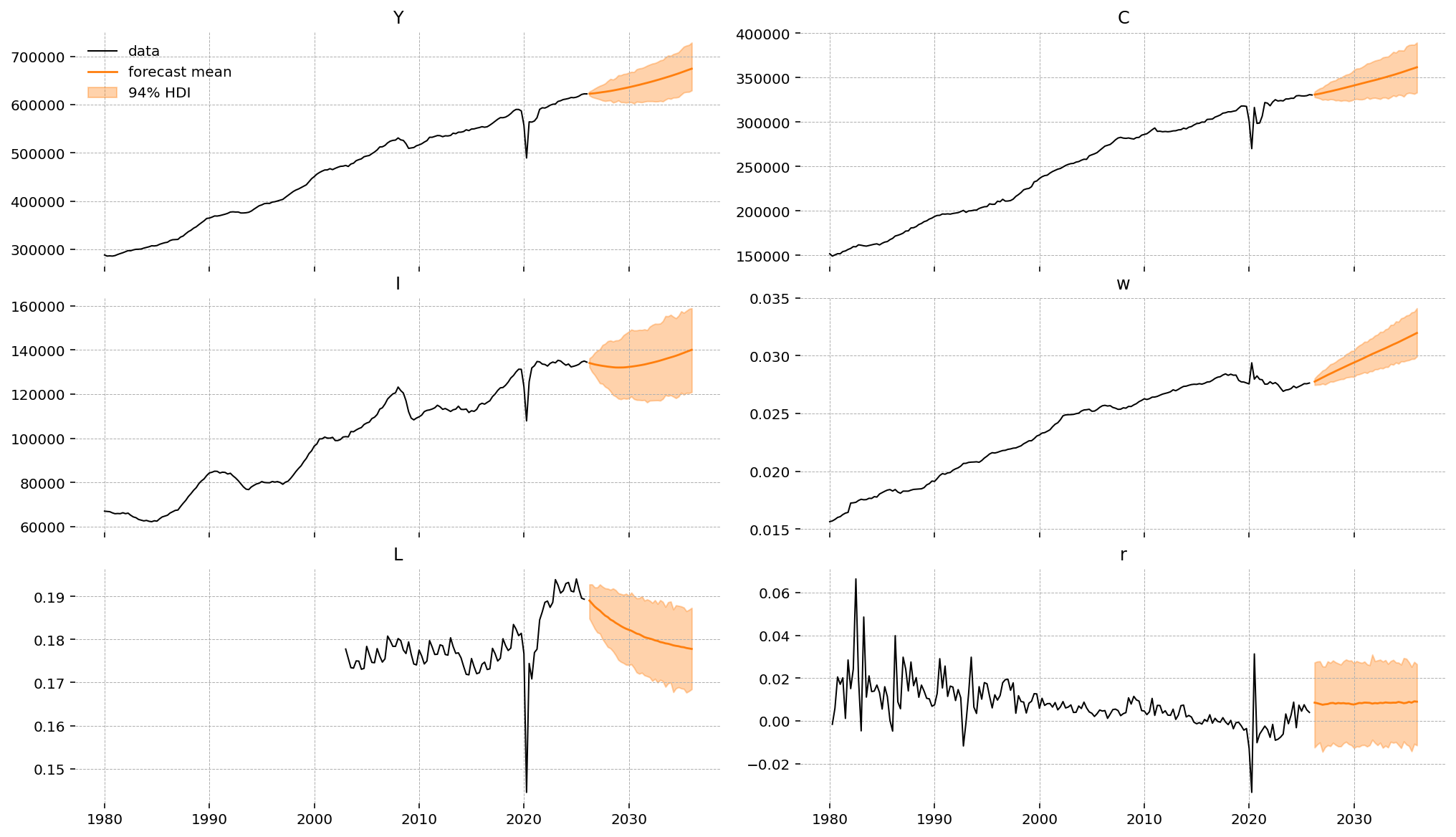

Forecasting#

The state-space machinery makes forecasting essentially free: given any starting time in the sample (and the joint posterior over parameters and states), it propagates the linear transition forward and samples observation paths. For our growth model, the forecasts are already in the right units — the four dlog_* paths come out as quarterly real growth rates and log_L, r come out in their observation scales. No retrending step is needed because the model’s own \(g_z\) and \(\varepsilon_z\) trend dynamics are baked into the prediction.

Below we forecast forty quarters (ten years) from five quarters before the end of the sample, so we can compare the in-sample tail to the model’s mean / 95% credible interval.

forecast = ss_mod.forecast(idata, periods=40, start=df_obs.index[-1], random_seed=rng)

/Users/jessegrabowski/mambaforge/envs/geconpy-dev/lib/python3.12/site-packages/pymc_extras/statespace/utils/data_tools.py:179: ImputationWarning: Provided data contains missing values and will be automatically imputed as hidden states during Kalman filtering.

warnings.warn(impute_message, ImputationWarning)

Sampling: [forecast_combined]

# Each observable maps to a raw series in `df` and an inverse transform:

# "growth" -- data is a log-difference; re-trend by anchoring at the last

# observed level and cumulating: X_T * exp(cumsum(dlog)).

# "log" -- data is a log level; invert with exp.

# "level" -- data is already in model units; identity.

obs_meta = {

"dlog_Y": ("Y", "growth"),

"dlog_C": ("C", "growth"),

"dlog_I": ("I", "growth"),

"dlog_W": ("w", "growth"),

"log_L": ("L", "log"),

"R_f": ("r", "level"),

}

fc = forecast.forecast_observed # (chain, draw, time, observed_state)

fc_time = fc.coords["time"].values

start = df_obs.index[-1]

fig, axes = plt.subplots(3, 2, figsize=(14, 8), sharex=True, layout="constrained")

for ax, name in zip(axes.flat, ss_mod.observed_states, strict=False):

raw_col, kind = obs_meta[name]

series = fc.sel(observed_state=name)

# Invert the preprocessing transform *per draw*, before taking any

# summaries -- cumulating must happen draw-by-draw, not on the HDI bounds.

if kind == "growth":

level = df[raw_col].ffill().loc[start] * np.exp(series.cumsum(dim="time"))

elif kind == "log":

level = np.exp(series)

else:

level = series

mu = level.mean(dim=["chain", "draw"])

hdi = az.hdi(level)

data = df[raw_col]

ax.plot(data.index, data.values, color="black", lw=1.0, label="data")

ax.plot(fc_time, mu.values, color="tab:orange", lw=1.4, label="forecast mean")

ax.fill_between(fc_time, *hdi.values.T, color="tab:orange", alpha=0.35, label="94% HDI")

ax.set_title(raw_col)

axes.flat[0].legend(frameon=False)

plt.show()

Authors#

Created by Jesse Grabowski, May 21, 2026

Watermark#

%load_ext watermark

%watermark -n -u -v -iv -m -w

Last updated: Thu, 21 May 2026

Python implementation: CPython

Python version : 3.12.13

IPython version : 9.13.0

Compiler : Clang 19.1.7

OS : Darwin

Release : 25.4.0

Machine : arm64

Processor : arm

CPU cores : 14

Architecture: 64bit

arviz : 1.1.0

arviz_plots: 1.1.0

eurostat : 1.1.1

gEconpy : 2.1.1.dev11+gdd1b3ddcc.d20260521

jax : 0.10.1

matplotlib : 3.10.9

numpy : 2.4.6

nutpie : 0.16.10

pandas : 3.0.3

preliz : 0.25.0

pymc : 6.0.0

pytensor : 3.0.2

Watermark: 2.6.0