Choosing a Sparse Root Solver#

gEconpy provides several solvers for nonlinear systems with sparse Jacobians. All of them are used through

one function, sparse_root, which accepts a solver instance. This notebook walks through the available

solvers, shows how to configure them, and compares their behavior on problems of increasing difficulty.

The objective function must return a tuple (residuals, jacobian), where the residual is an ndarray

and the Jacobian is a scipy sparse matrix.

import time

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import scipy.sparse as sp

from gEconpy.plotting import set_matplotlib_style

from gEconpy.solvers.sparse_root import (

Chord,

GaussNewtonTrustRegion,

InexactNewtonKrylov,

LevenbergMarquardt,

NewtonArmijo,

NewtonNonmonotone,

SparseDogleg,

sparse_root,

)

set_matplotlib_style()

Test Problems#

We define three test problems. The first is a small system to demonstrate the API. The second and third are large sparse systems where solver choice actually matters.

def quadratic(x):

"""x^2 - [1, 4] = 0. Solution at [1, 2]."""

return x**2 - np.array([1.0, 4.0]), sp.diags(2 * x, format="csc")

def broyden_tridiagonal(x):

"""Broyden tridiagonal system. Classic large sparse test problem."""

n = len(x)

res = (3.0 - 2.0 * x) * x + 1.0

res[:-1] -= 2.0 * x[1:]

res[1:] -= x[:-1]

jac = sp.diags(

[-np.ones(n - 1), 3.0 - 4.0 * x, -2 * np.ones(n - 1)],

[-1, 0, 1],

format="csc",

)

return res, jac

def trigonometric(x):

"""Trigonometric system (More, Garbow, Hillstrom). Many near-solutions."""

n = len(x)

sumcos = np.sum(np.cos(x))

idx = np.arange(1, n + 1, dtype=np.float64)

res = float(n) - sumcos + idx * (1.0 - np.cos(x)) - np.sin(x)

diag_vals = (1.0 + idx) * np.sin(x) - np.cos(x)

off_diag = np.sin(x)

J_dense = np.tile(off_diag, (n, 1))

np.fill_diagonal(J_dense, diag_vals)

jac = sp.csc_matrix(J_dense)

return res, jac

Basic Usage#

With no solver argument, sparse_root defaults to Newton’s method with Armijo backtracking. This is

a good general-purpose choice.

Success: True

Solution: [1. 2.]

Iterations: 5

To choose a different solver, pass an instance to the solver argument.

result = sparse_root(quadratic, np.array([2.0, 3.0]), solver=LevenbergMarquardt(), progressbar=False)

print(f"Success: {result.success}, iterations: {result.nit}")

Success: True, iterations: 5

The Solvers#

The solvers fall into two families.

Line-search solvers compose a direction strategy with a globalization strategy. They are constructed via factory functions:

NewtonArmijo()— exact Newton direction + Armijo backtrackingChord()— reuses the Jacobian for several steps, reducing factorization costInexactNewtonKrylov()— solves the Newton system approximately via GMRES, good for very large systemsNewtonNonmonotone()— allows the merit function to increase temporarily, helping escape narrow valleys

Trust-region solvers manage their own step acceptance:

SparseDogleg()— Powell dogleg within an adaptive trust regionGaussNewtonTrustRegion()— Gauss-Newton with Steihaug-CG subproblem solverLevenbergMarquardt()— damped Gauss-Newton with adaptive \(\lambda\)

Let’s compare all seven on the Broyden tridiagonal system at \(n = 1000\).

solvers = {

"NewtonArmijo": NewtonArmijo(),

"Chord": Chord(),

"InexactNewtonKrylov": InexactNewtonKrylov(),

"NewtonNonmonotone": NewtonNonmonotone(),

"SparseDogleg": SparseDogleg(),

"GaussNewtonTR": GaussNewtonTrustRegion(),

"LevenbergMarquardt": LevenbergMarquardt(),

}

n = 1000

x0 = -np.ones(n)

rows = []

for name, solver in solvers.items():

t0 = time.perf_counter()

result = sparse_root(broyden_tridiagonal, x0.copy(), solver=solver, progressbar=False)

elapsed = time.perf_counter() - t0

rows.append(

{

"solver": name,

"success": result.success,

"iterations": result.nit,

"f_evals": result.nfev,

"max |residual|": f"{np.max(np.abs(result.fun)):.2e}",

"time (ms)": f"{elapsed * 1000:.1f}",

}

)

pd.DataFrame(rows).set_index("solver")

| success | iterations | f_evals | max |residual| | time (ms) | |

|---|---|---|---|---|---|

| solver | |||||

| NewtonArmijo | True | 5 | 6 | 6.66e-16 | 7.9 |

| Chord | True | 8 | 9 | 4.37e-11 | 2.3 |

| InexactNewtonKrylov | True | 8 | 9 | 2.11e-13 | 4.1 |

| NewtonNonmonotone | True | 5 | 6 | 6.66e-16 | 1.5 |

| SparseDogleg | True | 7 | 8 | 7.77e-16 | 2.6 |

| GaussNewtonTR | True | 7 | 8 | 1.11e-15 | 4.1 |

| LevenbergMarquardt | True | 5 | 6 | 2.51e-13 | 2.9 |

Composing Direction and Globalization Strategies#

The line-search solvers are built from two interchangeable pieces:

A direction strategy computes the search direction at each step

A globalization strategy chooses how far to step in that direction

The factory functions pick sensible defaults, but you can mix and match. For example, here we pair a Krylov direction (iterative linear solve) with a nonmonotone line search:

from gEconpy.solvers.sparse_root.direction import KrylovDirection

from gEconpy.solvers.sparse_root.globalization import NonmonotoneBacktracking

from gEconpy.solvers.sparse_root.line_search import LineSearchSolver

custom_solver = LineSearchSolver(

direction=KrylovDirection(krylov_method="gmres"),

globalization=NonmonotoneBacktracking(memory=10),

)

result = sparse_root(broyden_tridiagonal, -np.ones(1000), solver=custom_solver, progressbar=False)

print(f"Success: {result.success}, iterations: {result.nit}")

Success: True, iterations: 8

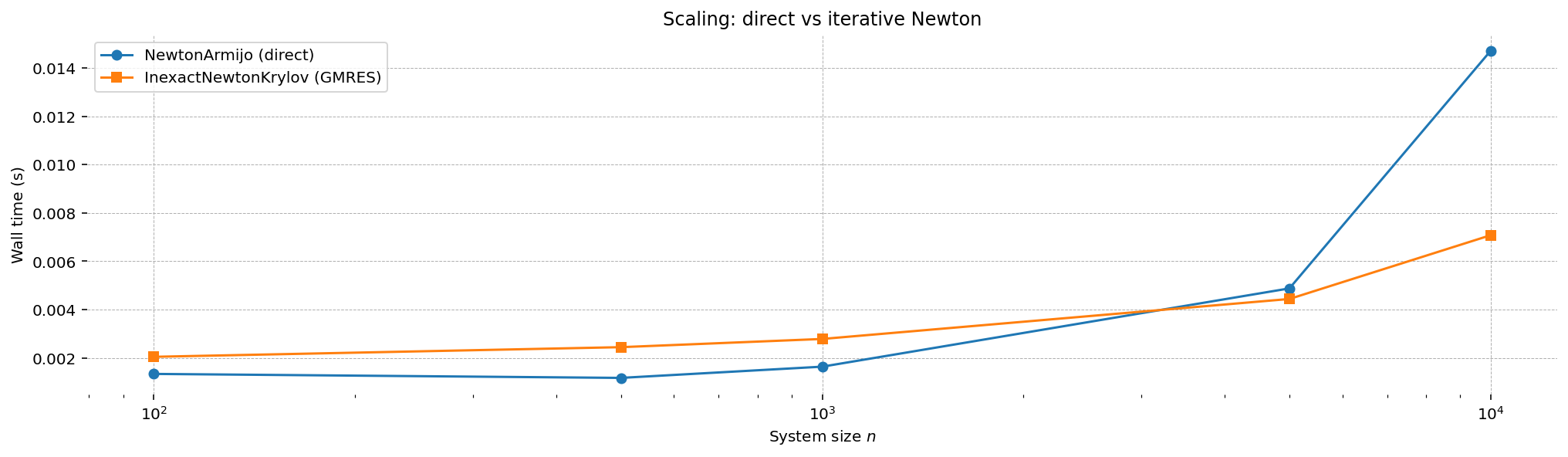

Scaling: Krylov vs Direct Solvers#

For large systems, the Jacobian factorization in NewtonArmijo can become the bottleneck.

InexactNewtonKrylov avoids factorization entirely by solving the Newton system iteratively. Let’s see

how they scale on the Broyden tridiagonal system as \(n\) grows.

sizes = [100, 500, 1_000, 5_000, 10_000]

newton_times = []

krylov_times = []

for n in sizes:

x0 = -np.ones(n)

t0 = time.perf_counter()

sparse_root(broyden_tridiagonal, x0.copy(), solver=NewtonArmijo(), progressbar=False)

newton_times.append(time.perf_counter() - t0)

t0 = time.perf_counter()

sparse_root(broyden_tridiagonal, x0.copy(), solver=InexactNewtonKrylov(), progressbar=False)

krylov_times.append(time.perf_counter() - t0)

fig, ax = plt.subplots()

ax.plot(sizes, newton_times, "o-", label="NewtonArmijo (direct)")

ax.plot(sizes, krylov_times, "s-", label="InexactNewtonKrylov (GMRES)")

ax.set_xlabel("System size $n$")

ax.set_ylabel("Wall time (s)")

ax.set_title("Scaling: direct vs iterative Newton")

ax.legend()

ax.set_xscale("log")

plt.show()

Difficult Problems: Trigonometric System#

The Moré-Garbow-Hillstrom trigonometric system has many near-solutions and is hard for monotone line-search methods. Trust-region and nonmonotone solvers tend to do better here.

n = 50

x0 = np.ones(n) / n

rows = []

for name, solver in solvers.items():

result = sparse_root(trigonometric, x0.copy(), solver=solver, progressbar=False, maxiter=500)

rows.append(

{

"solver": name,

"success": result.success,

"iterations": result.nit,

"f_evals": result.nfev,

"max |residual|": f"{np.max(np.abs(result.fun)):.2e}",

}

)

pd.DataFrame(rows).set_index("solver")

| success | iterations | f_evals | max |residual| | |

|---|---|---|---|---|

| solver | ||||

| NewtonArmijo | True | 11 | 38 | 2.64e-13 |

| Chord | True | 28 | 217 | 5.00e-11 |

| InexactNewtonKrylov | False | 500 | 7658 | 1.05e-03 |

| NewtonNonmonotone | True | 9 | 10 | 4.61e-11 |

| SparseDogleg | True | 290 | 346 | 4.87e-04 |

| GaussNewtonTR | True | 34 | 70 | 8.48e-04 |

| LevenbergMarquardt | True | 28 | 50 | 7.00e-04 |

Tuning Solver Parameters#

All solvers expose their parameters as constructor arguments. Here are a few examples.

Armijo parameters: c1 controls how much decrease the line search demands. Smaller values are more

permissive (accept steps more readily); larger values are stricter.

from gEconpy.solvers.sparse_root.globalization import ArmijoBacktracking

loose = NewtonArmijo(globalization=ArmijoBacktracking(c1=1e-6))

strict = NewtonArmijo(globalization=ArmijoBacktracking(c1=0.5))

x0_far = np.full(1000, 100.0)

r_loose = sparse_root(broyden_tridiagonal, x0_far.copy(), solver=loose, progressbar=False)

r_strict = sparse_root(broyden_tridiagonal, x0_far.copy(), solver=strict, progressbar=False)

print(f"Loose c1=1e-6: {r_loose.nit} iterations, {r_loose.nfev} f-evals")

print(f"Strict c1=0.5: {r_strict.nit} iterations, {r_strict.nfev} f-evals")

Loose c1=1e-6: 7 iterations, 8 f-evals

Strict c1=0.5: 15 iterations, 31 f-evals

Chord recompute frequency: the Chord solver reuses the Jacobian factorization for several steps,

trading accuracy for speed. The recompute_every parameter controls this tradeoff.

from gEconpy.solvers.sparse_root.direction import ChordDirection

rows = []

for freq in [1, 3, 5, 10, 20]:

solver = Chord(direction=ChordDirection(recompute_every=freq))

result = sparse_root(broyden_tridiagonal, -np.ones(1000), solver=solver, progressbar=False)

rows.append({"recompute_every": freq, "iterations": result.nit, "success": result.success})

pd.DataFrame(rows).set_index("recompute_every")

| iterations | success | |

|---|---|---|

| recompute_every | ||

| 1 | 5 | True |

| 3 | 7 | True |

| 5 | 8 | True |

| 10 | 12 | True |

| 20 | 21 | True |

Levenberg-Marquardt damping: the initial damping parameter \(\lambda_0\) controls how cautious the first steps are. Too large and the solver crawls; too small and it may overshoot.

rows = []

for lam0 in [1e-6, 1e-3, 1.0, 100.0]:

solver = LevenbergMarquardt(lam0=lam0)

result = sparse_root(broyden_tridiagonal, -np.ones(1000), solver=solver, progressbar=False)

rows.append({"lam0": lam0, "iterations": result.nit, "f_evals": result.nfev, "success": result.success})

pd.DataFrame(rows).set_index("lam0")

| iterations | f_evals | success | |

|---|---|---|---|

| lam0 | |||

| 0.000001 | 5 | 6 | True |

| 0.001000 | 5 | 6 | True |

| 1.000000 | 8 | 9 | True |

| 100.000000 | 12 | 13 | True |

Cheap Merit Evaluation with merit_fun#

During backtracking, the line-search solvers evaluate the objective function at every trial step to

check the Armijo condition. By default this calls the full fun, which computes both residuals and

the Jacobian — even though the Jacobian is only needed at the finally accepted point.

When the Jacobian is expensive (as in large stacked DSGE systems), this is wasteful. You can pass a

merit_fun to the globalization strategy that returns only the residuals. The solver will use it

for all trial evaluations during backtracking, then call the full fun once at the accepted point to

obtain the Jacobian.

def broyden_residuals_only(x):

"""Residuals without the Jacobian — much cheaper to evaluate."""

len(x)

res = (3.0 - 2.0 * x) * x + 1.0

res[:-1] -= 2.0 * x[1:]

res[1:] -= x[:-1]

return res

solver_with_merit = NewtonArmijo(globalization=ArmijoBacktracking(merit_fun=broyden_residuals_only))

result = sparse_root(broyden_tridiagonal, -np.ones(1000), solver=solver_with_merit, progressbar=False)

print(f"Success: {result.success}, iterations: {result.nit}, f_evals: {result.nfev}")

Success: True, iterations: 5, f_evals: 11

The solver converges to the same solution but avoids computing the Jacobian at every rejected trial point. The benefit grows with system size and Jacobian cost — in perfect foresight simulation (below), the Jacobian involves assembling a block-tridiagonal sparse matrix across hundreds of time periods, so skipping it during backtracking is a significant win.

Application: Perfect Foresight Simulation#

In practice, these solvers are used under the hood by ge.solve_perfect_foresight. A perfect foresight

simulation stacks the model equations across all time periods into one large sparse nonlinear system.

The size of that system grows linearly with the simulation length, so solver choice matters.

solve_perfect_foresight automatically compiles a residual-only version of the stacked system and

attaches it as the merit_fun on the solver’s globalization strategy. You don’t need to do anything

— the optimization described in the previous section is applied for you whenever the default

NewtonArmijo solver is used, or whenever you pass a line-search solver with an ArmijoBacktracking

or NonmonotoneBacktracking globalization strategy.

Let’s start with the RBC model using defaults, then switch to the larger New Keynesian model with a custom solver.

RBC model with defaults#

import gEconpy as ge

rbc = ge.model_from_gcn(ge.data.get_example_gcn("RBC"), verbose=False)

T = 500

shock = np.zeros(T)

shock[0] = 0.05

trajectory, result = ge.solve_perfect_foresight(rbc, simulation_length=T, shocks={"epsilon_A": shock})

print(f"Success: {result.success}, iterations: {result.nit}")

Success: True, iterations: 3

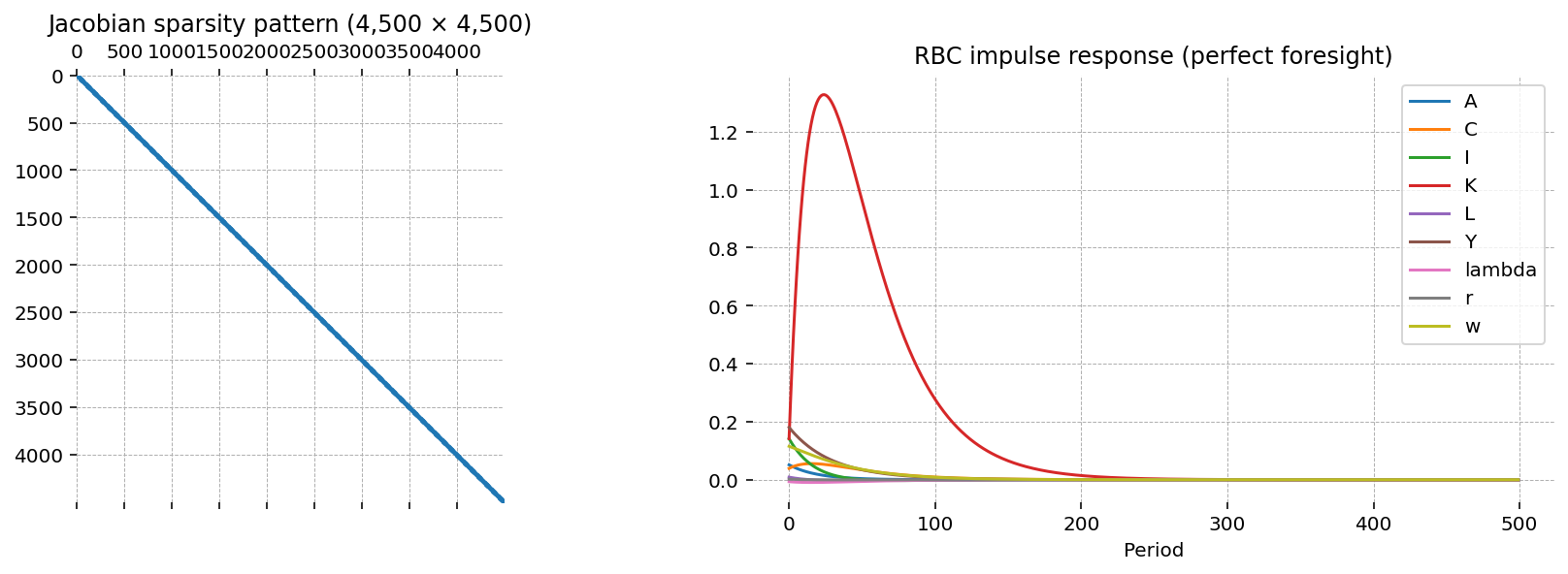

The system solved here has \(T \times n_{\text{vars}}\) unknowns. Let’s look at how big that is, and how sparse the Jacobian is at the solution:

n_vars = len(rbc.variables)

print(f"{'Variables per period:':25} {n_vars}")

print(f"{'Simulation length:':25} {T}")

print(f"{'Total unknowns:':25} {T * n_vars:,}")

print(f"{'Jacobian shape':25} {result.jac.shape}")

print(f"{'Jacobian nonzeros:':25} {result.jac.nnz:,}")

print(f"{'Density:':25} {result.jac.nnz / np.prod(result.jac.shape):.6%}")

Variables per period: 9

Simulation length: 500

Total unknowns: 4,500

Jacobian shape (4500, 4500)

Jacobian nonzeros: 15,492

Density: 0.076504%

fig, axes = plt.subplots(1, 2, figsize=(12, 4))

axes[0].spy(result.jac, markersize=0.05)

axes[0].set_title(f"Jacobian sparsity pattern ({result.jac.shape[0]:,} × {result.jac.shape[1]:,})")

steady_state = pd.Series({k.removesuffix("_ss"): v for k, v in rbc.steady_state().items()})

(trajectory - steady_state).plot(ax=axes[1], legend=True)

axes[1].set_xlabel("Period")

axes[1].set_title("RBC impulse response (perfect foresight)")

plt.show()

The Jacobian has a banded structure — each period’s equations only depend on variables at \(t-1\), \(t\), and \(t+1\). This is why sparse solvers are essential: a dense factorization of a matrix this size would be extremely expensive.

New Keynesian model with a custom solver#

The New Keynesian model has more variables per period (sticky prices, sticky wages, monetary policy),

so the stacked system is considerably larger. Here we use LevenbergMarquardt, a trust-region solver

that adapts its damping parameter \(\lambda\) each step.

nk = ge.model_from_gcn(ge.data.get_example_gcn("New_Keynesian"), verbose=False)

T_nk = 300

shock_nk = np.zeros(T_nk)

shock_nk[0] = 0.01

trajectory_nk, result_nk = ge.solve_perfect_foresight(

nk, simulation_length=T_nk, shocks={"epsilon_R": shock_nk}, solver=LevenbergMarquardt()

)

print(f"Success: {result_nk.success}, iterations: {result_nk.nit}")

Success: True, iterations: 13

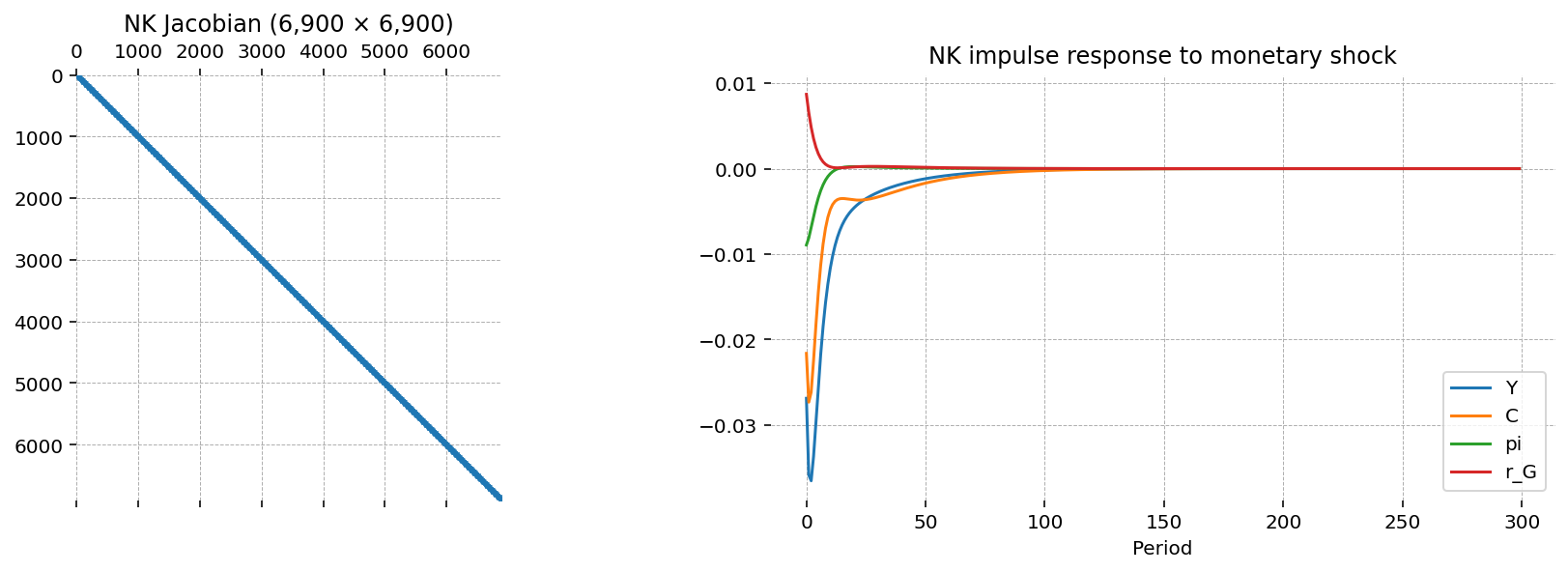

n_vars_nk = len(nk.variables)

print(f"{'Variables per period:':25} {n_vars_nk}")

print(f"{'Simulation length:':25} {T_nk}")

print(f"{'Total unknowns:':25} {T_nk * n_vars_nk:,}")

print(f"{'Jacobian shape':25} {result_nk.jac.shape}")

print(f"{'Jacobian nonzeros:':25} {result_nk.jac.nnz:,}")

print(f"{'Density:':25} {result_nk.jac.nnz / np.prod(result_nk.jac.shape):.6%}")

Variables per period: 23

Simulation length: 300

Total unknowns: 6,900

Jacobian shape (6900, 6900)

Jacobian nonzeros: 31,764

Density: 0.066717%

fig, axes = plt.subplots(1, 2, figsize=(12, 4))

axes[0].spy(result_nk.jac, markersize=0.02)

axes[0].set_title(f"NK Jacobian ({result_nk.jac.shape[0]:,} × {result_nk.jac.shape[1]:,})")

steady_state_nk = pd.Series({k.removesuffix("_ss"): v for k, v in nk.steady_state().items()})

(trajectory_nk - steady_state_nk)[["Y", "C", "pi", "r_G"]].plot(ax=axes[1])

axes[1].set_xlabel("Period")

axes[1].set_title("NK impulse response to monetary shock")

plt.show()

Authors#

Authored by Jesse Grabowski in March 2026, with assistance from Claude Opus 4.6

Watermark#

%load_ext watermark

%watermark -n -u -v -iv -w -p gEconpy

Last updated: Sun, 15 Mar 2026

Python implementation: CPython

Python version : 3.12.13

IPython version : 9.11.0

gEconpy: 2.0.4.dev37+g9a1a488f7.d20260315

gEconpy : 2.0.4.dev37+g9a1a488f7.d20260315

matplotlib: 3.10.8

numpy : 2.4.2

pandas : 3.0.1

scipy : 1.17.1

Watermark: 2.6.0